{kind=link}

In the post-Assad era, Syria is witnessing a noticeable wave of openness to investment, reflected in the announcement of a series of memoranda of understanding (MoUs) with international partners. While the figures announced point to highly ambitious goals, important questions arise regarding the practical mechanisms of implementation, the governing legal frameworks, and the factors that could determine whether these agreements remain at the level of intentions or materialize into tangible projects.

This study examines two sets of investment memoranda: 20 MoUs signed with international actors, analyzed individually by value, sector, geography, and timeline; and 47 initial agreements and MoUs, signed at once at the Syrian-Saudi Investment Forum in July 2025, worth USD 6.4 billion. Due to the lack of project details, these are assessed only by sector and overall value.

Group One: The Twenty MoUs—The Reality of Agreements in the Post-War Phase

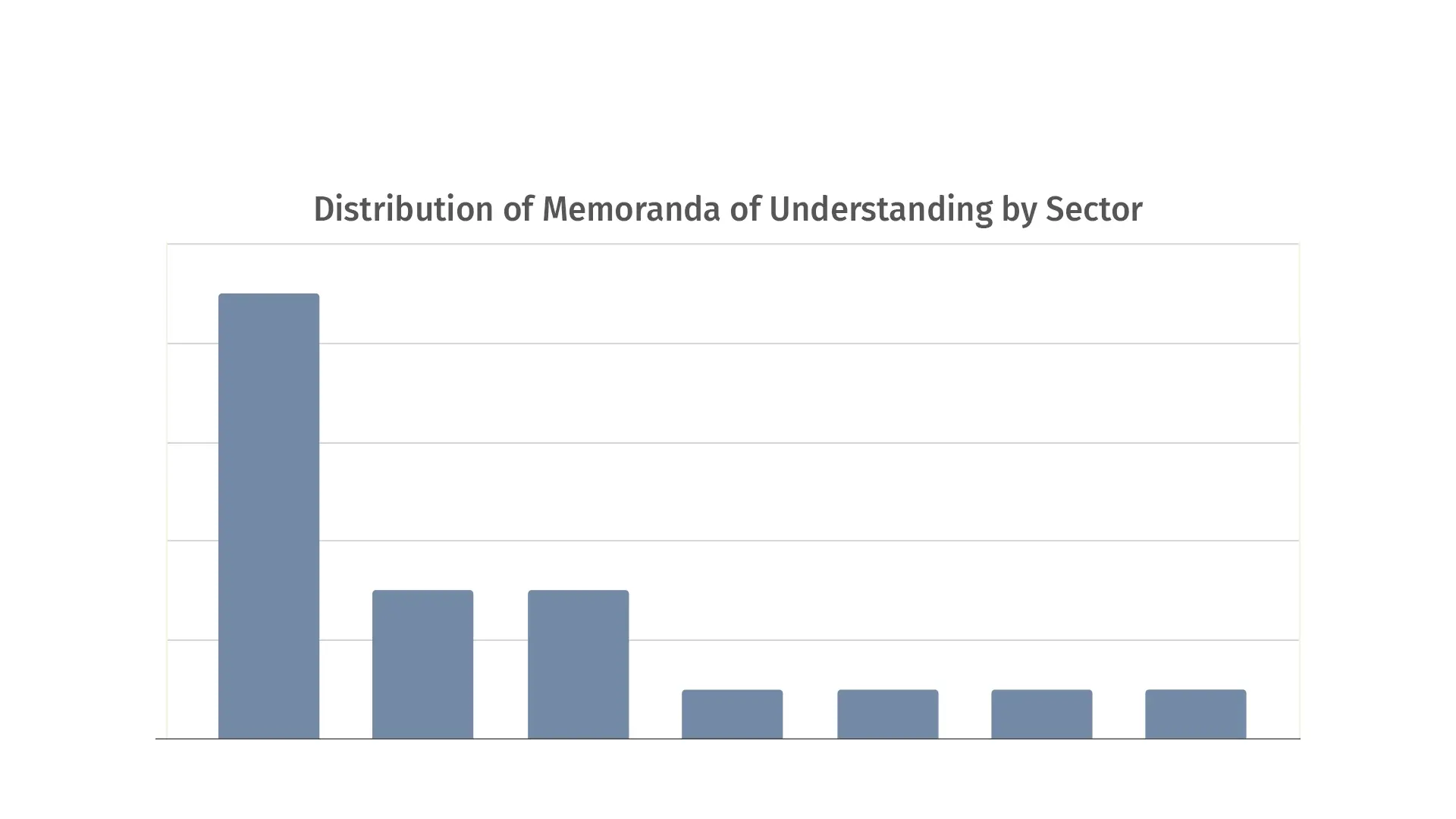

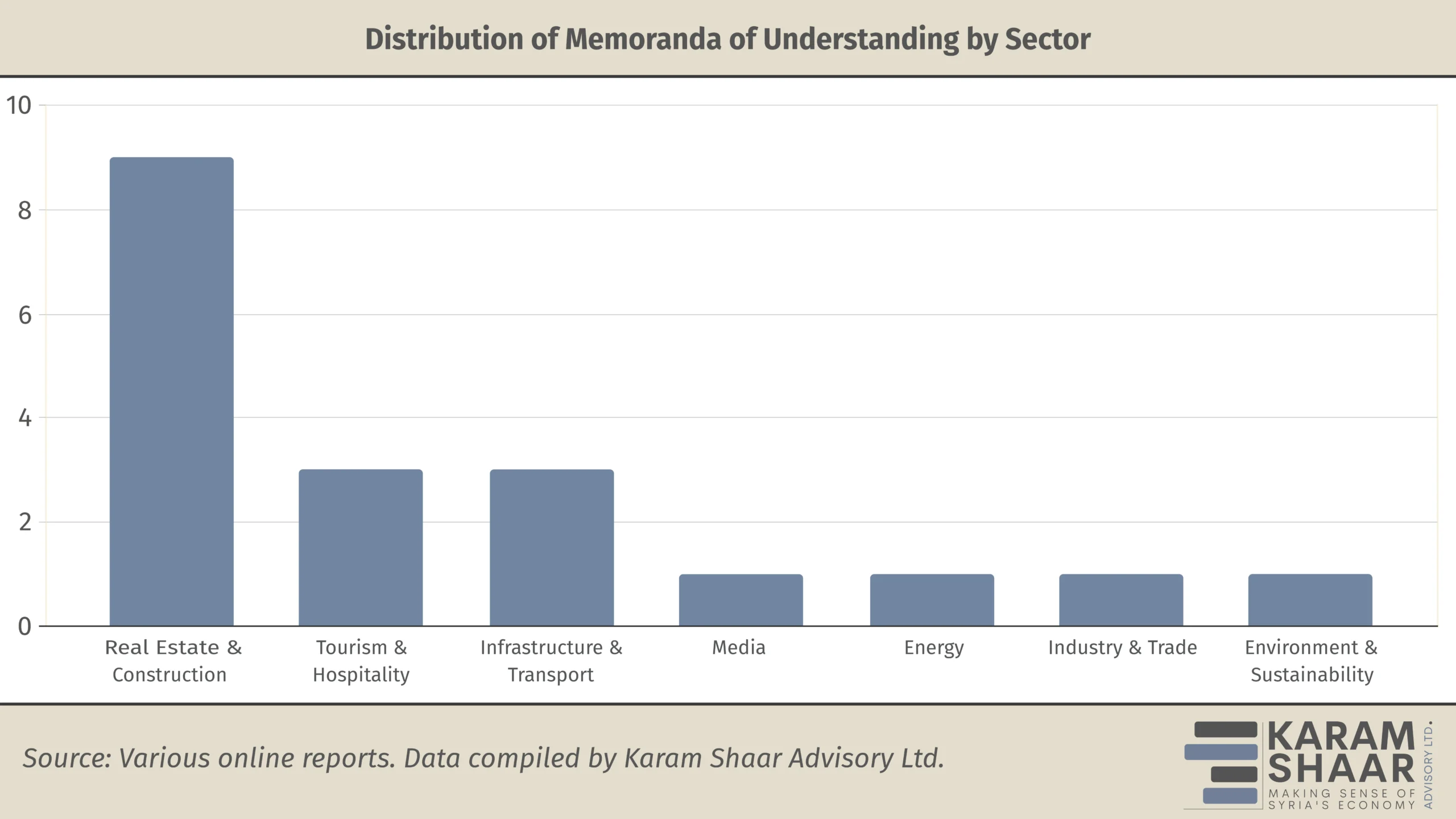

Since the downfall of the Assad regime, we have tracked 20 MoUs announced between Syrian state institutions and foreign companies. The values of 15 of these agreements were disclosed, amounting to a total of USD 19 billion; no details were provided for the remaining five. Collectively, these agreements span a wide range of sectors, with a strong focus on real estate and construction.

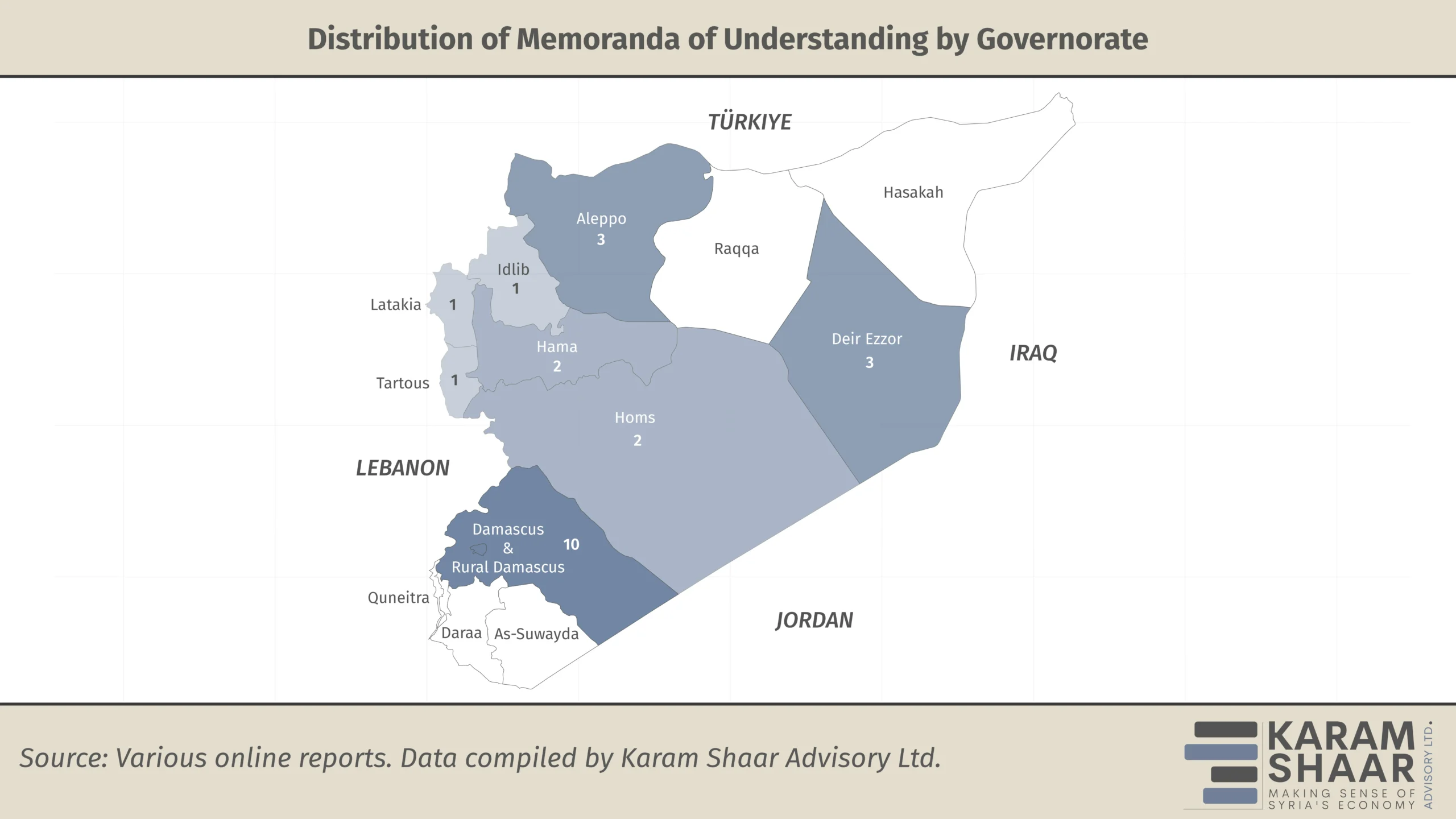

From a geographical perspective, the MoUs are spread across several provinces, with the primary concentration in Damascus and its countryside. Notably, Idlib Governorate—formerly the main stronghold of the current government—received only a single MoU. This could be read as a positive signal that the government does not intend to discriminate against previously contested areas, but it may also reflect a preference to keep Idlib’s future development more tightly under its own control, limiting external involvement at this stage.

Available information also indicates that many of the foreign partners involved in these agreements are newly established companies, raising questions about their technical and financial capacities to implement projects of this magnitude. While parties to MoUs often strive to present the highest degree of professionalism at the time of signing—with an embedded interest in exaggerating their capabilities—this may create an impression of seriousness that does not necessarily reflect actual implementation capabilities. The next issue of Syria in Figures will examine these companies through an interactive map of MoU signatories and their corporate ties.

Group Two: Agreements from the Syrian-Saudi Investment Forum

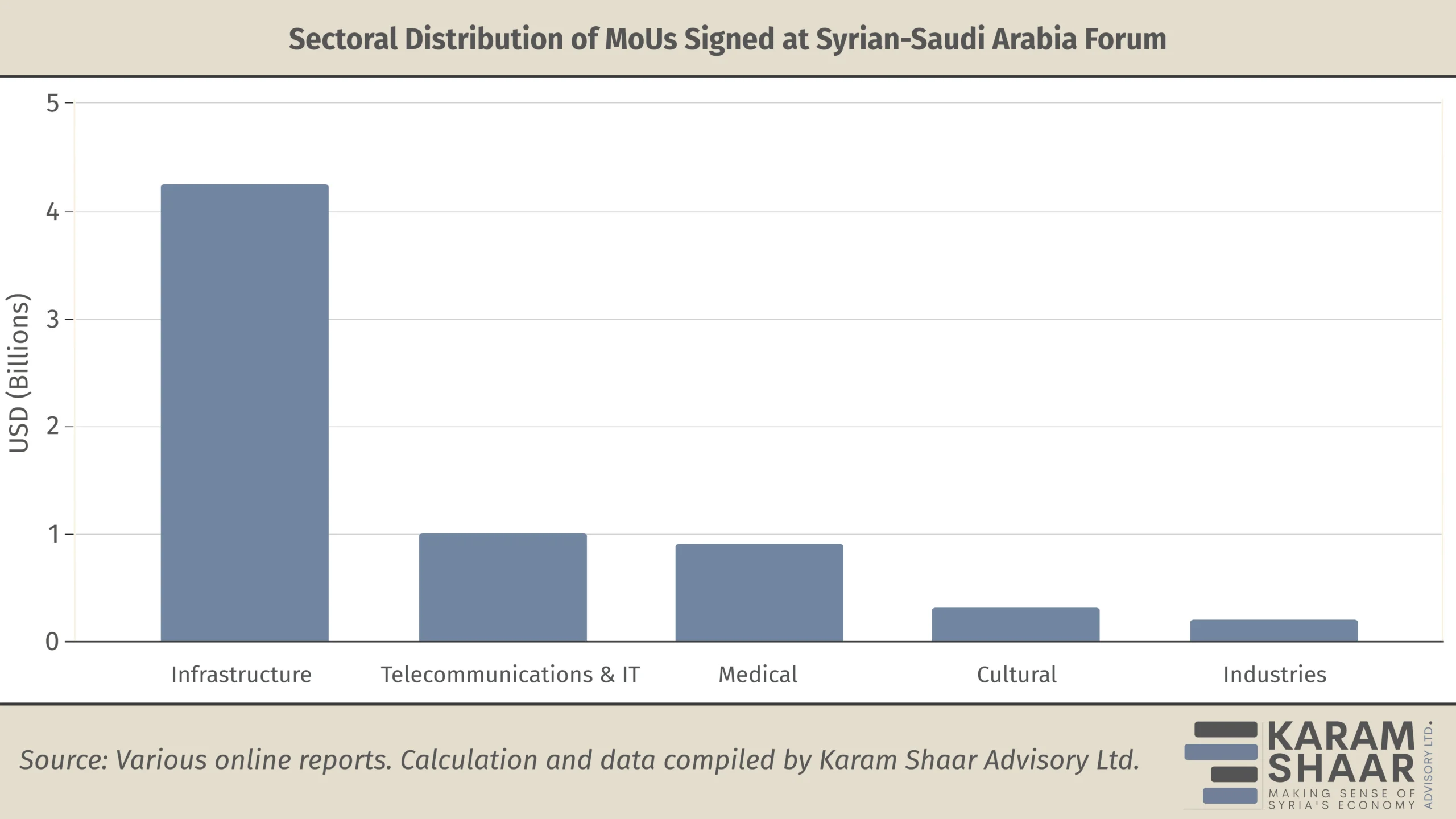

On 24 July 2025, the Syrian-Saudi Investment Forum was launched in Damascus with the participation of a high-level Saudi delegation headed by Minister of Investment Khalid Al-Falih. During the forum, 47 initial agreements and MoUs—were signed between several Syrian state institutions and Saudi companies, with a total value of USD 6.4 billion. Due to the inability to distinguish MoUs from these initial agreements according to the announcement, we treat all of them as MoUs.

The agreements cover infrastructure and real estate development, which accounted for the largest share of total investments, in addition to telecommunications and information technology, industry, tourism, and health. However, given the lack of disclosure on project nature and provincial distribution, we were unable to independently verify the geographic spread.

Implementation and Obstacles

Tracking the MoUs —including those concluded during the Syrian-Saudi Investment Forum—reveals that the actual rate of implementation has been extremely limited. Out of all the monitored memoranda, only one project has publicly commenced: the rehabilitation and development of production lines at the Fayhaa Cement Plant.

The short timeframe since the first agreements (just four months since the initial MoU with China’s Fidi Contracting) may partly explain the low implementation rate—particularly as the largest batch of MoUs was signed less than a month ago. The Syrian case, however, raises broader questions about whether such announcements can realistically move from paper to practice. To better understand what conditions enable MoUs to translate into actual investments, it is useful to compare Syria’s experience with that of neighboring countries where similar agreements were signed and implemented at scale. The Sharm el-Sheikh Economic Conference in Egypt in March 2015 offers a potential comparison.

At that conference, Egypt announced USD 72.5 billion in agreements, which included USD 36.2 billion in direct investments (final contracts) and USD 29 billion in MoUs—USD 12.7 billion in real estate and tourism, and USD 16.3 billion in electricity generation—in addition to USD 3.3 billion in cash support from the Gulf. Remarkably, work started on more than half of these projects within five months, thanks to political stability, direct Gulf financial support, and the existence of a clear institutional framework for implementation.

In Syria, however, structural obstacles to implementation are considerable. Security risks remain acute in several regions, with sporadic clashes continuing in the west, east, and south, along with a persistent, albeit waning, threat of terrorism. Such instability discourages long-term investment, while political and institutional uncertainty further complicates matters, as large projects are often launched without the transparency in bidding that major investors expect.

Sanctions and financial isolation add another layer of difficulty. Even with partial easing of the Caesar Act, much of the sanctions’ impacts remain in place, sustaining an environment of legal and financial uncertainty (see our newly launched monthly Syria Sanctions Monitor). At the same time, local banks remain disconnected from the global financial system, making cross-border transfers and capital flows extremely difficult.

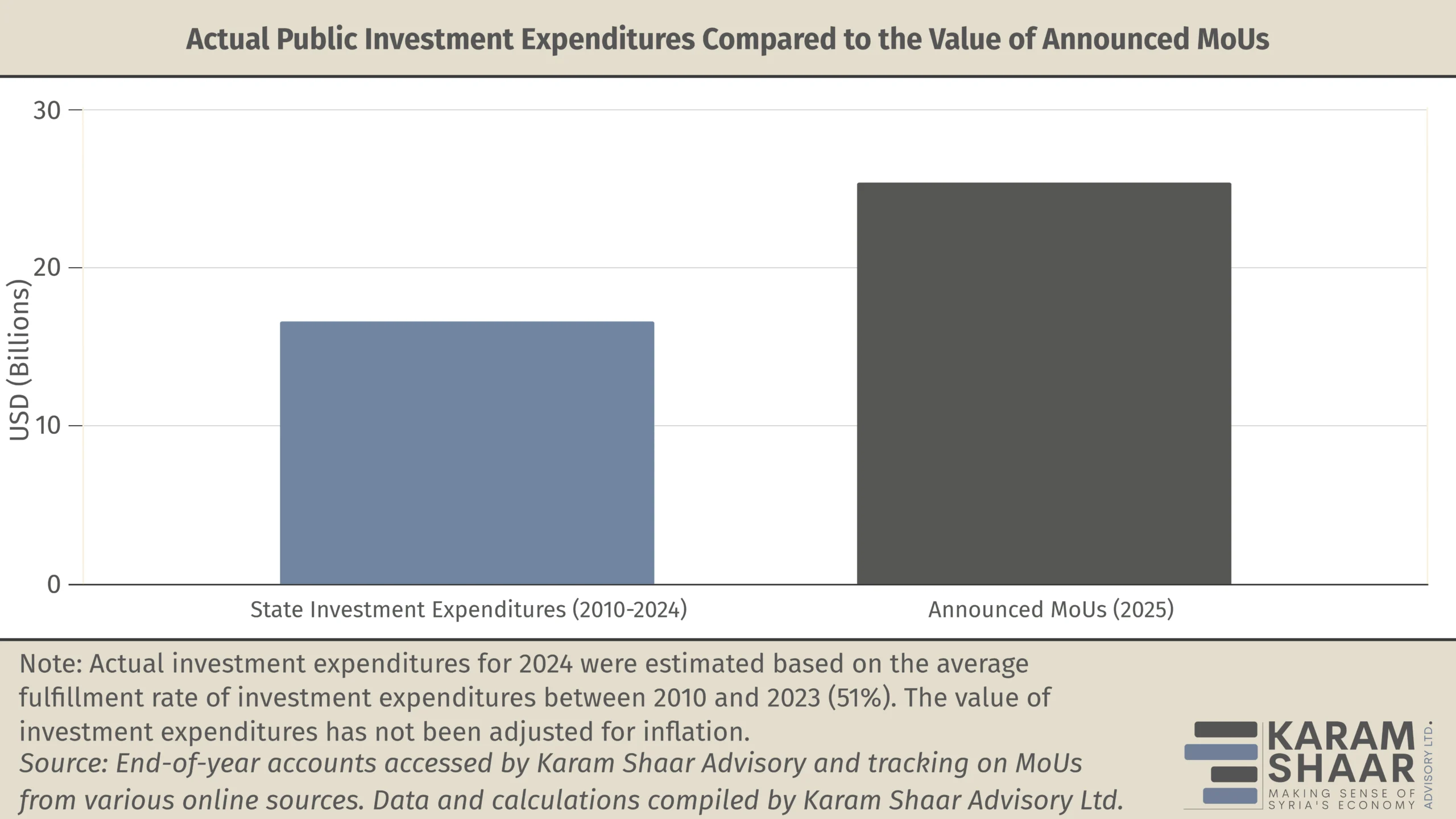

Finally, the scale of announced investments far exceeds Syria’s underlying economic capacity. To put the value of MoUs (USD 25.4 billion) into perspective, total government investment expenditures between 2010 and 2024 stood at USD 16.6 billion (see chart below). Foreign direct investment (FDI) figures for most of this period are unavailable, except for 2010 and 2011, but it is likely that FDI was minimal in subsequent years due to the deteriorated economic environment—and thus dwarfed by the value of recent announcements.

This stark imbalance raises serious questions about whether Syria has the institutional and financial capacity to absorb and manage projects of this scale, particularly after years of shrinking budgets and depleted state resources. Should these agreements materialize, however, they would have a transformational economic impact. World Bank data put Syria’s entire GDP in 2023 at only USD 20 billion.

Ways Forward

The signing of these MoUs demonstrates clear political intent, especially from Saudi Arabia and Qatar, while placing responsibility squarely on the Syrian government. Its next moves will be decisive—both for advancing the agreements and for shaping how investors and foreign governments judge its seriousness in pursuing recovery.

International engagement can add real weight if it strengthens regulatory capacity, clarifies legal frameworks, and reduces uncertainty for investors. Foreign policymakers should also recognize that Syria’s transition will be uneven. Still, early conditional signals of support—anchored in accountability and inclusivity—could steer reforms toward broad-based recovery rather than narrow short-term gains.