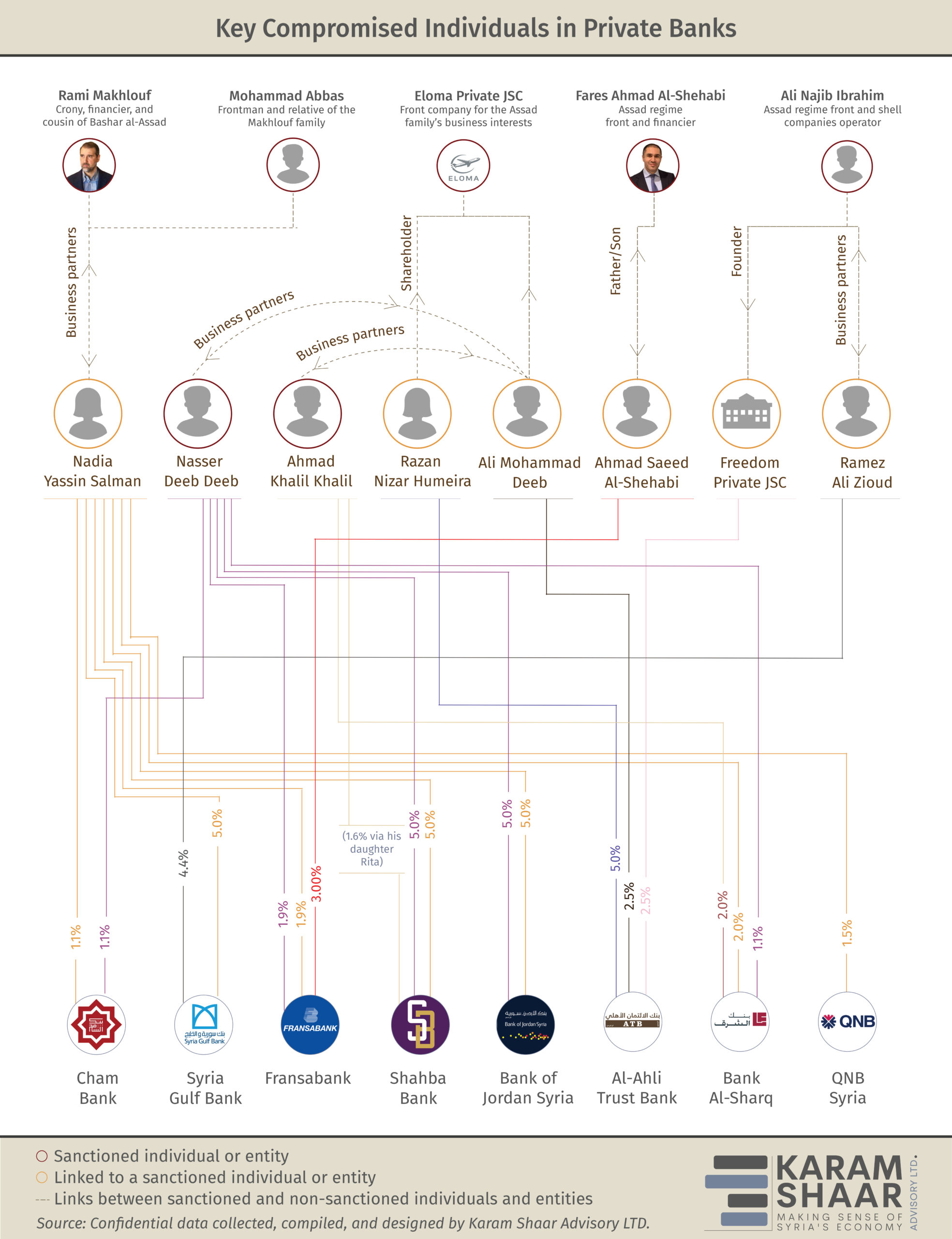

Among the most challenging figures to reconcile with from a compliance standpoint are Ahmad Khalil Khalil and Nasser Deeb Deeb, both directly sanctioned by the EU for acting as business frontmen for the Assad regime.

Ahmad Khalil Khalil holds direct stakes in Bank Al-Sharq (2.0%) and indirect stakes through his daughter Rita in Shahba Bank (1.6%). Together with his daughters, Rana and Rita, Khalil is widely recognized as a central figure in a network of shell companies, based on our review of the Official Gazette, many of which are tied to sanctioned actors or regime cronies. He is also the co-founder of Sanad Protection Services, a company with close ties to Russia’s Wagner Group, previously active in Syria.

Nasser Deeb Deeb, sanctioned for being the co-founder of Sanad Protection Services and for his alleged involvement in the captagon trade, also presents a particularly difficult compliance case. He holds shares in at least five banks—Cham Bank (1.1%), Fransabank (1.2%), Shahba Bank (5.0%), Bank of Jordan Syria (5.0%), and Bank Al-Sharq (1.1%). His name consistently appears in shareholder registries of institutions considered shells for the regime’s economic interests. At the same time, his stakes appear to have been systematically transferred from Ehab Makhlouf, Rami Makhlouf’s brother, on 18 November 2020, according to our review of shareholding changes, suggesting a possible link between the two.

By being both sanctioned and entrenched in the former regime’s economic networks, Khalil and Deeb present significant barriers to external re-engagement. In line with EU law, entities can be treated as sanctioned not only when designated persons hold 50% or more of ownership, but also when they exercise effective control or decisive influence. This means that even minority shareholders acting as a front for powerful sanctioned actors can cast a long shadow over compliance assessments and discourage international partnerships.

Moreover, with FATF guidance, correspondent banks must understand “who the beneficial owner(s) of the respondent institution is/are” and “require customer relationships to be terminated where identified risks cannot be managed.” While this does not outright prohibit correspondent banking where sanctioned individuals are involved, higher risks drive up compliance costs—already a barrier to establishing correspondent relations—and further erode commercial incentives to maintain or establish new relationships with banks in high-risk countries such as Syria.

Another seemingly compromised individual is Nadia Yassin Salman, a shareholder in seven Syrian banks (see chart above). While not directly sanctioned, since 6 June 2021 our review of shareholding structures has shown a systemic pattern: Rami Makhlouf’s shares disappear, and Nadia Yassin Salman’s appear in similar amounts. This happened following Rami Makhlouf’s downfall. She also seems to have taken over the shares of a Mohammad Hassan Abbas—a US-designated proxy for Rami Makhlouf—in the company “STC Specialized in Transportation Projects,” according to our review of the Official Gazette. These moves could indicate either an attempt to shield Rami Makhlouf’s assets or a regime-orchestrated transfer to a trusted proxy—placing her in a questionable position in either case.

…But a System-wide Problem

Beyond these two names, a broader cast of sanctioned individuals, politically exposed persons, and affiliated entities dominate shareholder registries across the banking sector, making international re-engagement increasingly complex.

At Al-Ahli Trust Bank (ATB), three shareholders illustrate the problem. Razan Nizar Humeira (4.5%) is a principal shareholder in Eloma Investment Private JSC (also written as Iloma), a company sanctioned by the EU, and has been involved in creating front companies with regime-aligned and sanctioned actors; her dealings show a deliberate pattern of obfuscation and proximity to Assad.

Ali Mohammad Deeb (2.5%) is similarly entrenched and has engaged in joint ventures with Ahmad Khalil Khalil and Nasser Deeb Deeb, including through sanctioned entities, based on our review of the Official Gazette.

Ali Najib Ibrahim—a sanctioned individual and a key figure in the Khalil/Deeb shell-company network—remains a principal actor in Freedom Private JSC, a holding company with equity in ATB.

Other individuals raise potential compliance concerns through familial or business associations. Nisreen Hussein Ibrahim, who owns shares in Al-Baraka Bank Syria, is individually sanctioned by the US and is the sister of Assad’s leading front Yassar Hussein Ibrahim. Ramez Ali Ziyoud, a shareholder in Syria Gulf Bank (4.4%), is not directly sanctioned but is linked to Ali Najib Ibrahim. Similarly, Ahmad Saeed Al-Shehabi, tied to Fransabank (3.0%), is the father of EU-designated regime-aligned businessman Fares Al-Shehabi.

Context and Solutions

Under global compliance standards, even a small stake held by a sanctioned person could make a bank’s access to the international system more difficult.

However, this situation presents a structural dilemma. According to several banking professionals in Damascus, some sanctioned individuals cannot divest their stakes because their assets have been effectively frozen by the new authorities, though it is unclear by which state institution exactly. While some businessmen have reportedly settled their cases with authorities, this might not apply to all. In other instances, regime-linked shareholders have left the country, making transfers practically unfeasible. Multiple bankers in Damascus noted at the end of July that these individuals no longer participate in shareholder meetings or decision-making processes.

Another reality is easy to overlook: at least some of these stakes were never freely chosen by the banks themselves. Some shareholders are likely to have been imposed during the Assad era, often as part of coercive asset transfers orchestrated by the regime. When Rami Makhlouf’s holdings were seized during his fallout with Assad, large share blocks were reportedly redistributed to frontmen and loyalists, leaving banks with little say.

A way forward is for the Syrian judiciary or presidency to issue verdicts or edicts that formally freeze and confiscate these assets, supporting the revival of the banking sector. Private banks should lobby for such measures to protect the sector’s viability and signal a break from the past.