Syria’s location has long positioned it as a potential energy hub, placing its territory at the center of numerous proposed pipeline projects—some executed, others never materialized. This is the final article in a series building on earlier Syria in Figures pieces that examined the implications of the revival of the Arab Gas Pipeline (AGP) and the Iraq–Syria oil pipeline. It concludes by inviting a broader reassessment of Syria’s potential role in future regional gas transit networks.

Three pipelines are central to this discussion.

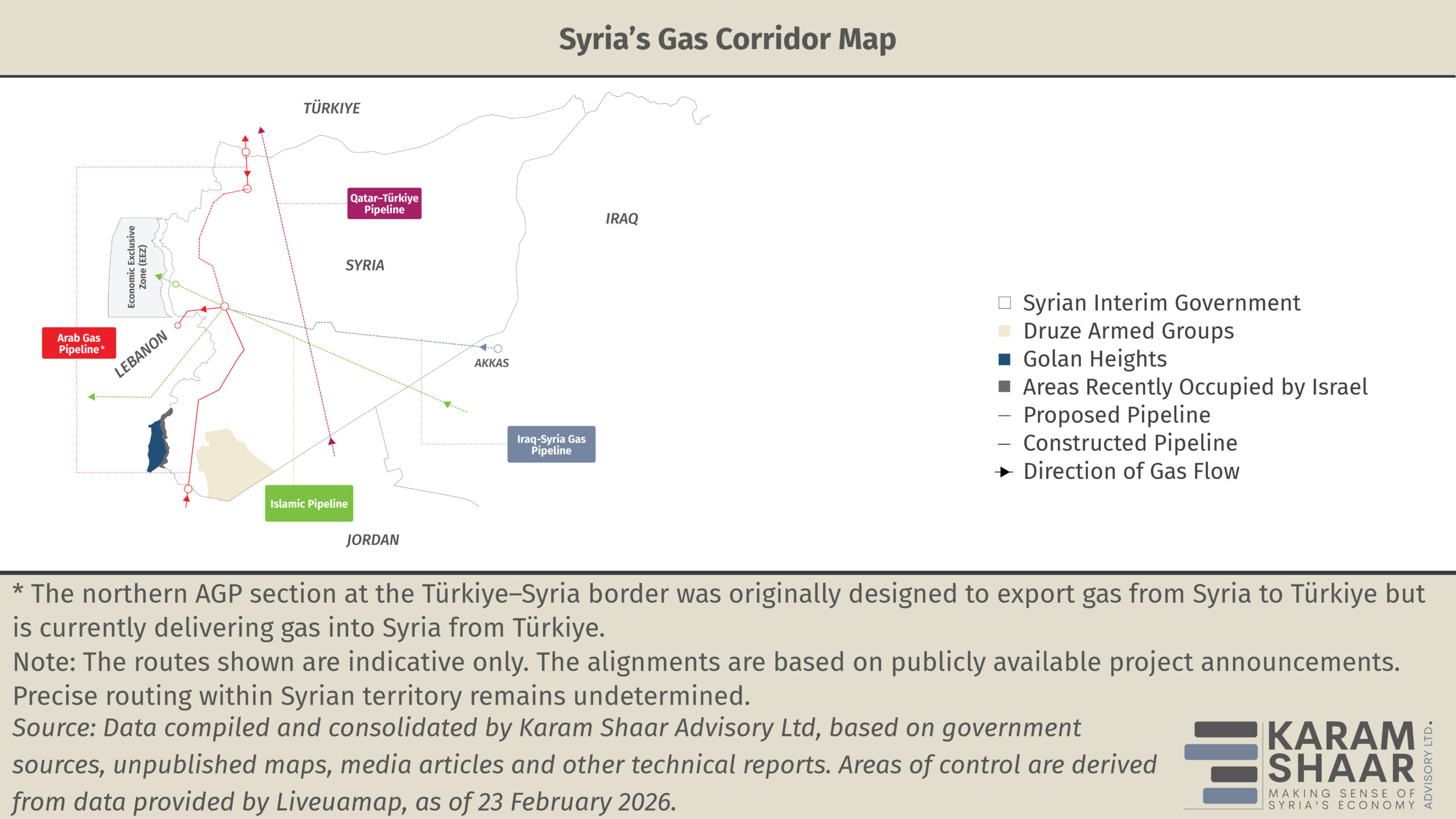

The first is the Qatar–Türkiye Gas Pipeline. Proposed in 2009 by Sheikh Hamad bin Khalifa Al Thani, then-ruler of Qatar, the project aimed to transport gas from Qatar’s North Field to Türkiye and onward to European markets. One potential route would have passed through Saudi Arabia, Jordan, and Syria before reaching Türkiye. This would have linked to the AGP and potentially offered an alternative to Russia’s natural gas supplies to Europe. The project was also promoted by then-Prime Minister Recep Tayyip Erdoğan. Former Syrian President Bashar al-Assad reportedly refused to sign the agreement in 2009, allegedly under pressure from Russia. Discussions about reviving the project resumed within 48 hours of Assad’s escape. Turkish Energy and Natural Resources Minister Alparslan Bayraktar stated that the pipeline could be realized if Syria restored its territorial integrity and achieved stability. However, Qatar firmly denied that any discussions were currently underway.

The second regional pipeline is the Friendship Pipeline, also known as the Islamic Pipeline. In July 2011, Iran, Iraq, and Syria signed a Memorandum of Understanding (MoU) for a similar gas project. In February 2013, Iraq approved the framework agreement for its construction. The pipeline was intended to transport Iranian natural gas from the South Pars field—shared with Qatar—through Iraq and Syria, potentially reaching Lebanon, Mediterranean ports, and ultimately Europe. The escalation of the Syrian conflict indefinitely delayed the proposed 5,600 km pipeline, whose cost was estimated at USD 10 billion. In 2021, Syria’s Minister of Electricity stated that the project had not been abandoned. Assad’s departure in December 2024, along with Iran’s diminished influence in Syria, effectively suspended it.

Third is the Akkas Gas Pipeline, sometimes referred to in the media as the Iraq–Europe Gas Pipeline. Planned as early as 2009, it aimed to connect the Akkas gas field in Iraq’s western al-Anbar province to European markets via Türkiye. The pipeline was also intended to connect with the AGP in Syria and function as an extension of the larger international Kirkuk–Homs Gas Pipeline. Escalating conflict in Syria and Iraq halted development agreements. ISIS seized the Akkas field in 2014, suspending operations and ultimately stalling the project. Sanctions on Syria posed additional obstacles. As the conflict subsided, signs of revival emerged. In mid-2024, reports indicated that the Iraqi government had awarded development of the Akkas field to an undisclosed Ukrainian company. In January 2026, drilling operations began under the leadership of the US-based company Schlumberger (SLB).

Against this historical backdrop, a different energy reality is taking shape. Since August 2025, Syria has been receiving gas from Azerbaijan’s Shah Deniz field via Türkiye, entering northern Syria through the Kilis–Aleppo pipeline, with Qatari financing. Plans are underway to extend the line southward to Homs, positioning Türkiye and Qatar as central actors in Syria’s immediate energy security. Syria’s demand for gas to generate electricity, combined with limited domestic output, makes such regional cooperation necessary.

A second operational corridor has emerged with the revival of the AGP. In January 2026, Syria began receiving around four million cubic meters of gas per day from Jordan. Egypt is also considering exporting approximately 1.8 million cubic meters per day to Lebanon via the same route. The gas Syria imports through Jordan is being regasified in Aqaba, Jordan, before being transported north. Much of it, however, is effectively Israeli in origin due to Jordan’s imports from the Leviathan field and regional swap arrangements. This creates a geopolitical paradox in which Syria and Lebanon rely on gas from a country they do not formally recognize.

Syria could theoretically receive gas from multiple sources through previously proposed projects while benefiting from existing infrastructure, particularly the operational AGP, which increases its exposure as a potential transit hub. In addition, restoring domestic production or making new discoveries within Syria’s Exclusive Economic Zone (EEZ) in the northern Levantine Basin could strengthen its position in the regional energy market.

In this context, statements by the head of the Syrian Petroleum Company (SPC), Youssef Qablawi, are notable. In late 2025, Qablawi outlined a vision in which Syria would double its domestic gas production in the short term and, by 2030, position itself as a regional hub exporting gas to Europe.

In practice, however, major obstacles hinder large-scale reintegration into regional energy networks. These include security requirements, substantial capital investment to rehabilitate damaged infrastructure, and the need for sustained political certainty. Regardless of projected profits, such conditions underpin any significant energy investment. Moreover, many of these pipeline concepts predate the expansion of gas production and exports from the eastern Mediterranean. The development of Israeli and Cypriot fields has reshaped the regional landscape, potentially reducing the relevance or urgency of earlier proposals.

The region also faces significant competition. Israel, Egypt, Cyprus and others are pursuing similar objectives through the Eastern Mediterranean Gas Forum (EMGF), potentially bypassing both Syria and Türkiye. Other competing initiatives include the Israel–Türkiye–EU Pipeline, the Kirkuk (Iraq)–Erzurum (Türkiye) gas pipeline, and the Persian Pipeline, which would extend from southern Iran to Türkiye and onward to Europe, bypassing Arab states including Syria. An additional alternative is the substitution of pipeline gas with liquefied natural gas (LNG), which may offer greater flexibility.

Following the collapse of the Assad regime in December 2024, Syria’s potential as an energy hub has regained attention. A critical distinction must nevertheless be made between a transit hub and a transit state. A hub shapes routes, pricing, and diversification; a transit state merely hosts infrastructure determined by external actors. Official discourse, including the SPC’s 2030 vision, aspires to the former. Yet current realities—Azerbaijani gas entering via Türkiye, Israeli-origin gas arriving through Jordan, and projects dependent on foreign capital—suggest the latter.