Harout Ekmanian

1. Introduction

Syria’s post-conflict trajectory presents both opportunities and uncertainties for foreign investors. The protection of foreign investment under international law becomes especially important in States afflicted by armed conflict and prolonged political instability, where the risk of expropriation, asset destruction, and regulatory disruption is materially elevated. Syria presents a particularly instructive case study in this regard. Over a decade of civil conflict has fundamentally altered its investment landscape, rendering the interplay between domestic legislation, bilateral investment treaties, and available international dispute resolution mechanisms both legally complex and practically significant. This brief focuses specifically on the international legal regime governing foreign investment protection, examining its efficacy and limitations.

Syria’s domestic investment regime has undergone successive reforms, from Law 10 of 1991 through Investment Law 18 of 2021, and most recently Decree 114 of 2025. The latter builds upon its predecessors by refining the scope of permissible investment, updating sector-specific incentives, and recalibrating applicable restrictions. Decree 114 now serves as the principal legislative instrument governing foreign investment. The Syrian Constitutional Declaration of 2025 provides baseline protections against expropriation and nationalization, while the Syria Investment Agency and relevant licensing authorities administer the approval and oversight of foreign investment projects.

Moreover, the government established new sovereign and development funds to channel reconstruction financing. It also signed billions of dollars in memoranda of understanding with Gulf, Turkish, and Western partners. Syria’s reconnection to the SWIFT system, engagement with the IMF and World Bank, and the significant easing of EU, UK, and US sanctions further facilitate reintegration into the global investment landscape. Two new international arbitration centers were established in Syria within the last few months, which will be discussed in this brief.

Thus, the transitional government under President Ahmad al-Sharaa seems to have signaled its commitment to attracting foreign capital. Notwithstanding these protections, the domestic legal framework retains notable limitations that, in a conflict-affected regulatory environment, underscore the importance of the supplementary international legal protections examined in the sections that follow.

2. International Treaty Framework

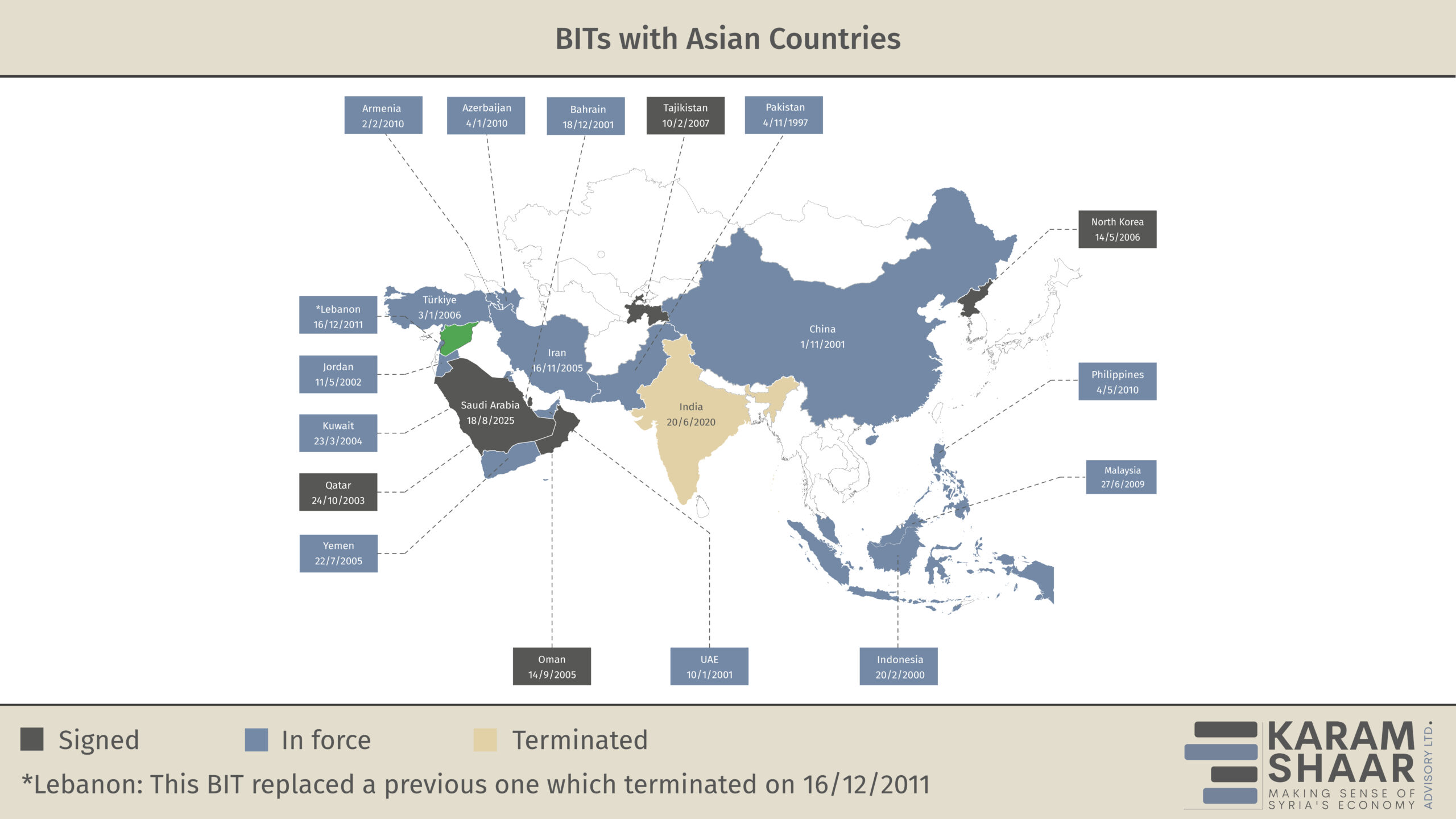

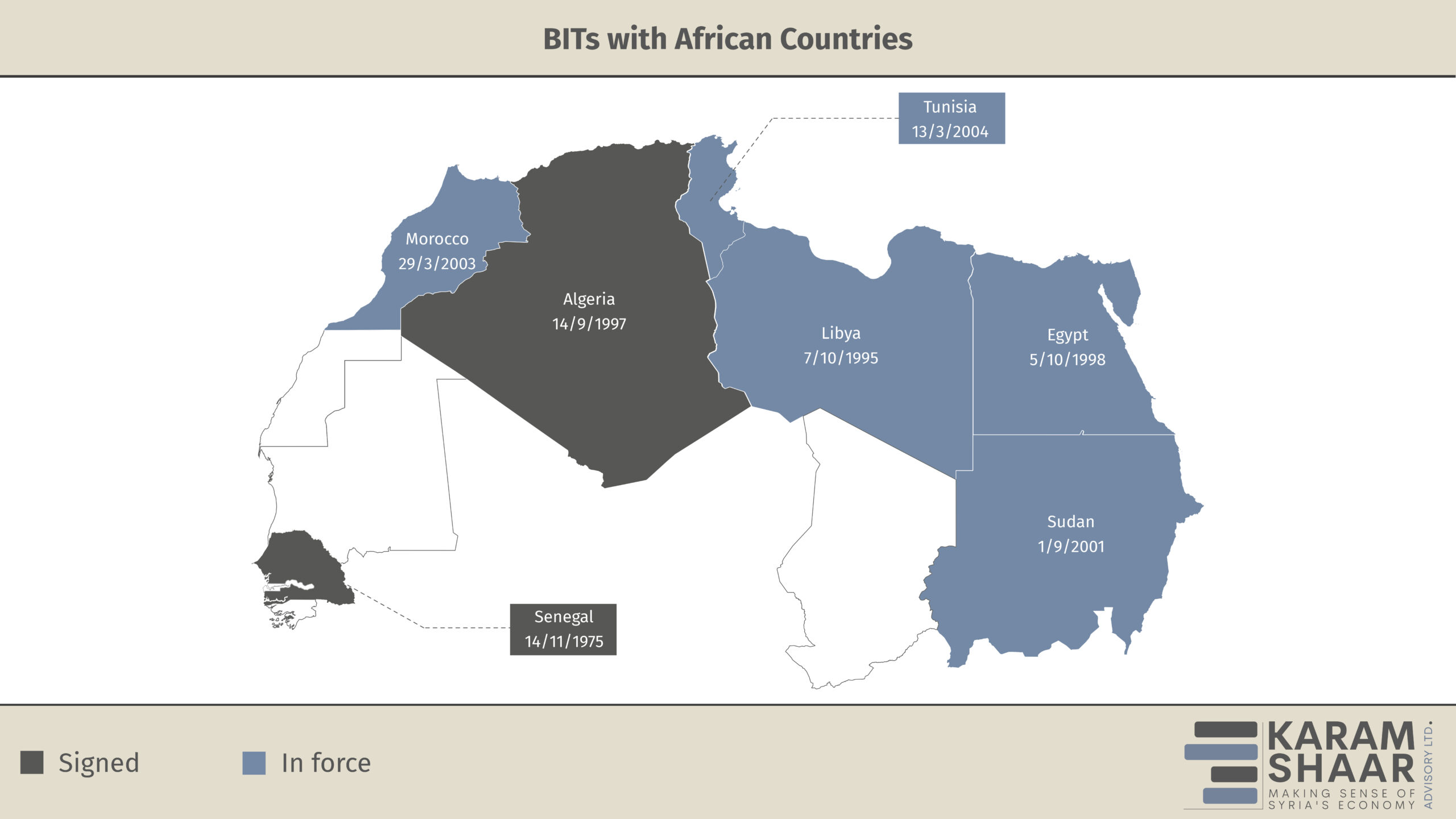

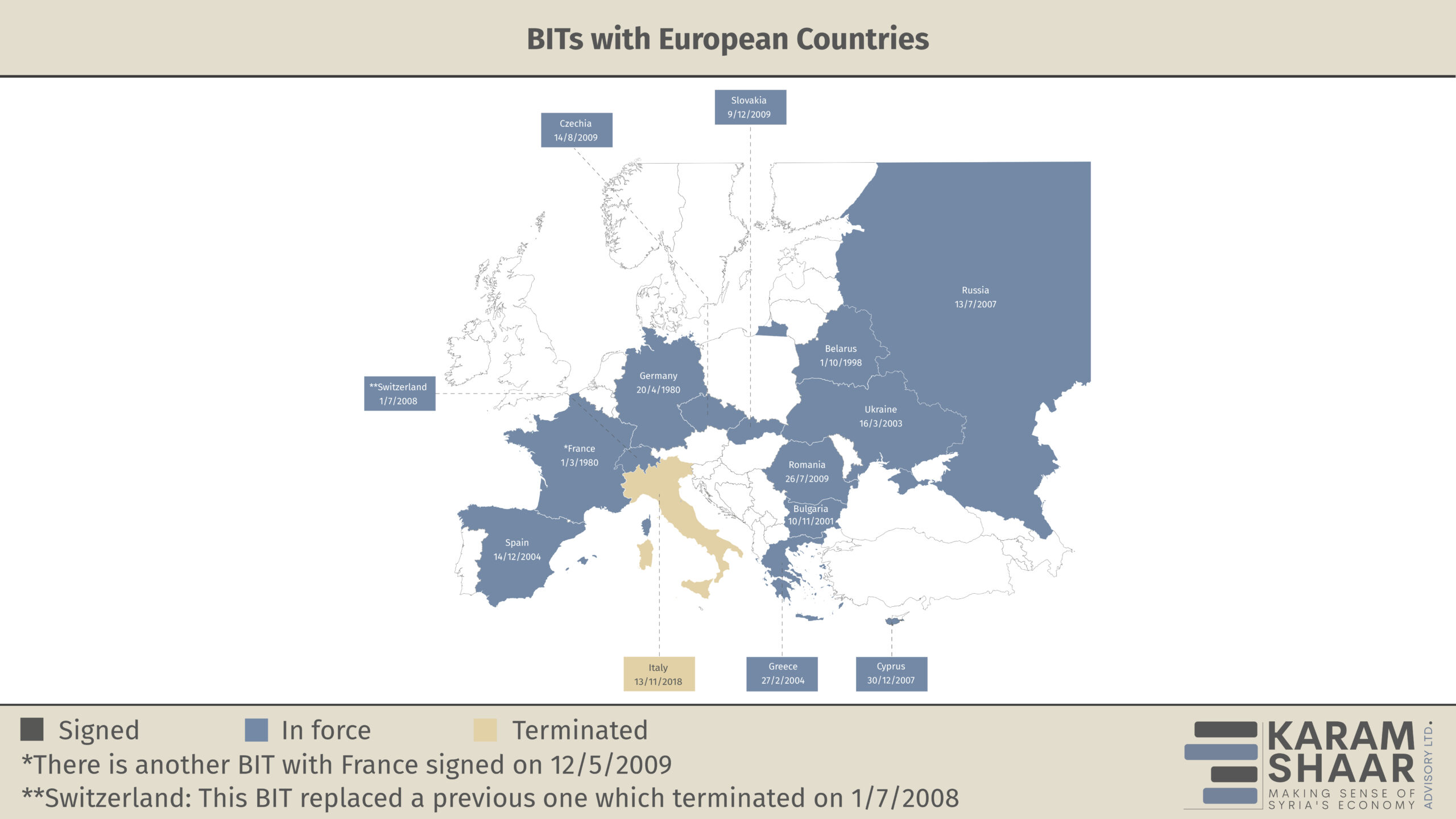

Syria has signed a total of 45 bilateral investment treaties (BITs), of which 33 are currently in force. Eight BITs remain signed but not ratified—including treaties with Senegal (1975), Algeria (1997), Qatar (2003), Oman (2005), North Korea (2006), Tajikistan (2007), France (2009), and most recently Saudi Arabia (2025)—while four have been terminated. Syria’s treaty partners span a broad geographic range, encompassing major European economies such as Germany, Switzerland, and Spain, as well as key regional counterparts including Türkiye, China, Russia, and numerous Arab and Gulf states. Beyond its BIT network, Syria is party to four multilateral treaties with investment provisions (TIPs), all currently in force: the Syria–Türkiye Free Trade Agreement (2004), the Agreement on Promotion, Protection and Guarantee of Investments amongst the Member States of the Organization of the Islamic Conference (OIC Investment Agreement) (1980), the Unified Agreement for the Investment of Arab Capital in the Arab States (1980), and the Arab League Investment Agreement (1970).

Syria has also ratified the Convention on the Settlement of Investment Disputes between States and Nationals of Other States (ICSID Convention), which provides an international framework for conciliation and arbitration of investment disputes between foreign investors and Contracting States. The convention entered into force for Syria on 24 February 2006.

Syria is also a party to the United Nations Convention on the Recognition and Enforcement of Foreign Arbitral Awards of 1958 (the New York Convention), which facilitates the enforcement of arbitral awards arising from investment disputes. Syria signed the convention in 1959 and remains bound by it today.

The standards of treatment (also referred to as substantive protections) afforded under Syria’s in-force BITs generally reflect standard international investment law provisions, though the precise language and scope vary from treaty to treaty and must be examined on a case-by-case basis. Most of these treaties guarantee fair and equitable treatment (FET), one of the most frequently invoked standards in investor-state disputes. Many also provide for full protection and security (FPS), ensuring the physical—and in some cases legal—protection of an investment, as well as protection against direct and indirect expropriation without prompt, adequate, and effective compensation.

Additional protections commonly found in Syria’s BITs include:

- the free transfer of funds, guaranteeing the repatriation of profits and dividends

- most-favored-nation (MFN) treatment, enabling investors to import more favorable substantive protections from other BITs in force with Syria

- national treatment (NT), which requires the host state to treat foreign investors no less favorably than domestic investors in like circumstances

- umbrella clauses, which can elevate contractual obligations of the host state (in this case, Syria) to the level of international obligations under the treaty (see Table A in the annex).

However, not all of Syria’s BITs contain the full complement of these protections, and certain treaties include limitations which will be discussed further below, such as denial-of-benefits clauses, essential security exceptions, or requirements to exhaust local remedies before resorting to international arbitration.

The standards of treatment most frequently engaged in conflict settings acquire particular salience in the Syrian context. Expropriation claims—whether arising from direct seizures, legislative takings, or the destruction of assets attributable to state conduct—require tribunals to distinguish compensable state action from collateral war damage, with indirect expropriation claims raising complex questions of causation and attribution.

FET assumes a distinctive character under conditions of state fragility: while investors retain legitimate expectations formed at the time of investment, tribunals may accord the State a wider margin of appreciation where the regulatory environment has been fundamentally disrupted by conflict. FPS acquires heightened relevance during armed conflict, as the physical security dimension of this standard is directly engaged; however, the obligation remains one of due diligence rather than strict liability, requiring only that the State take reasonable measures within its capacity to protect investments. The prohibition on non-impairment by unreasonable or discriminatory measures provides an additional avenue of recourse where state conduct, though falling short of expropriation, nonetheless materially undermines the investment through arbitrary or discriminatory treatment.

3. State Defenses and Exceptions

No standard of treatment automatically ceases to apply during armed conflict. However, the host state may invoke defenses such as the essential security exception, where present in BIT text. The Syrian government may argue that the impugned measures were necessary to protect its security. This defense operates as a threshold exception, meaning that the treaty’s substantive obligations do not apply in the circumstances covered by the exception.

Separately, under customary international law, Article 25 of the International Law Commission’s (ILC) 2001 Articles on Responsibility of States for Internationally Wrongful Acts permits a State to invoke necessity (i.e., it should not be held internationally responsible for breaching its treaty obligations) where the specific measure taken by the State is the only way to safeguard an essential interest against a grave and imminent peril.

The defense is available only where the State did not contribute to the situation of necessity—a narrowly construed defense, as the Argentine crisis jurisprudence (CMS, LG&E, Enron, Sempra) demonstrates.

Syria may also plead force majeure to justify noncompliance under Article 23 of the ILC Articles, arguing that the armed conflict constituted an irresistible force beyond its control rendering performance of treaty obligations materially impossible, though this defense is unavailable if the State contributed to the situation or assumed the risk of its occurrence. The Güriş v. Syria arbitration under the Syria-Türkiye BIT is, to date, one of the most significant publicly known cases testing these standards in the context of the Syrian conflict.

Beyond these substantive defenses, international sanctions regimes—historically imposed by the EU, the US, and the UN—have profoundly affected the practical landscape of investment arbitration involving Syria. Although the EU and US have significantly eased most economic sanctions on Syria as of mid-2025, residual restrictions remain in force targeting specific individuals, terrorist-designated entities, and certain sectors. Sanctions may affect investor standing where BIT legality clauses or denial-of-benefits provisions are invoked against sanctioned investors; may complicate arbitral proceedings through asset freezes, restrictions on legal services, and payment difficulties; and may impede enforcement of awards where national courts treat sanctions compliance as a matter of public policy under Article V(2)(b) of the New York Convention.

The removal of sanctions does not, in itself, create new treaty obligations. Rather, it removes a layer of regulatory impediment that had, in practice, rendered the exercise of treaty rights exceedingly difficult—if not impossible—for a significant class of investors.

As a threshold matter, Syria’s BITs were never formally terminated or suspended by operation of the sanctions regimes. The treaties remained in force as a matter of public international law throughout the conflict and sanctions period; what was impaired was their practical operability and the ability of covered investors to invoke their protections without running afoul of sanctions compliance obligations. The lifting of sanctions therefore operates as a de facto reactivation of the full range of BIT protections, enabling investors to once again rely on the dispute resolution mechanisms (principally, international arbitration) contained in these instruments.

4. Applicable Arbitral Forums

Although Syria ratified the ICSID Convention, only an estimated 18 of its 33 in-force BITs provide access to ICSID arbitration. Ad hoc arbitration under the United Nations Commission on International Trade Law (UNCITRAL) Arbitration Rules is also available as a procedural option in most of Syria’s BITs. The distinction between the two frameworks carries material consequences.

ICSID arbitration operates as a self-contained system under the ICSID Convention:

- It is delocalized, meaning it is not subject to the law of any arbitral or juridical seat (i.e., independent from any country’s legal system).

- Its awards are subject only to annulment by an ad hoc committee under Article 52 of the ICSID Convention. Annulment is available on only five grounds: improper tribunal constitution, manifest excess of powers, corruption, serious procedural departure, or failure to state reasons. These narrow grounds are designed to ensure procedural integrity rather than review the merits.

- ICSID Contracting States are obligated to recognize and enforce awards as if they were final judgments of their own courts, without recourse to the defenses available under the New York Convention.

UNCITRAL arbitration, by contrast, is:

- Subject to a juridical seat, rendering awards subject to the supervisory jurisdiction of the courts at that seat, including the possibility of set-aside on a variety of grounds available under the applicable national arbitration law. These grounds may include invalidity of the arbitration agreement, procedural unfairness or due process violations, excess of authority or jurisdiction, improper tribunal composition, breach of public policy, fraud or corruption, arbitrator misconduct or bias, or non-arbitrability when the subject matter cannot be settled by arbitration under the law of the seat (such as criminal charges, land disputes, or family law).

- Enforcement of UNCITRAL awards depends on the New York Convention. Article V permits national courts to refuse recognition on grounds such as public policy or the award having been set aside at the juridical seat. Such defenses against enforcement of arbitral awards are unavailable against ICSID awards.

Additionally, ICSID imposes a dual-investment requirement (the dispute must qualify as an “investment” under both the applicable BIT and Article 25 of the ICSID Convention), while UNCITRAL tribunals generally apply only the BIT definition. ICSID bars claims by dual nationals holding the nationality of the respondent state, a restriction not applicable under the UNCITRAL framework.

Beyond ICSID and UNCITRAL, a smaller subset of Syria’s BITs—estimated at four—provides for arbitration under International Chamber of Commerce (ICC) rules. This feature is characteristic of certain European BIT models, such as the French and Swiss treaties, both of which reflect arbitration-friendly legal traditions. In Güriş v. Syria, the claimants successfully accessed ICC arbitration despite the Syria-Türkiye BIT listing only ICSID and UNCITRAL. They did so by invoking the MFN clause to import the ICC option from Syria’s BIT with Italy, although that treaty had expired and was no longer in force.

In practice, this precedent significantly expands the range of available forums for investors under any Syrian BIT containing an MFN clause.

Another institutional option appearing sporadically across Syria’s BITs with several members of the League of Arab States is the Arab Investment Court, established by the Unified Agreement for the Investment of Arab Capital in the Arab States in 1980. However, the court has never become operational.

The practical implications of this procedural landscape are considerable: an investor’s choice of forum will determine not only the applicable procedural rules and degree of institutional support, but also the enforceability of any resulting award and the scope of available recourse against it.

5. Procedural Considerations and Other Issues

Investors potentially pursuing claims against the Syrian government may face significant jurisdictional hurdles at the threshold stage. Claimants must demonstrate qualification as protected investors under the applicable BIT, assessed by reference to criteria such as place of incorporation, seat of management, or nationality of controlling persons. This issue would be central to potential cases involving some recent agreements between the Syrian government and unverified corporate entities. International arbitration tribunals increasingly scrutinize corporate restructuring designed solely to gain BIT protections after a dispute becomes foreseeable. Therefore, investors should structure their investments with attention to potential treaty protection at an early stage and with appropriate legal advice.

From Syria’s perspective, denial-of-benefits clauses offer a critical defense, permitting the State to deny treaty protections to shell entities lacking substantial business activities in the home state. The dual-nationality bar under ICSID Article 25(2)(a) may further narrow the pool of eligible claimants.

The conduct of proceedings is further complicated by procedural challenges inherent to conflict zones, affecting both parties. Service of arbitral notices on Syrian state organs may prove difficult where institutions have been displaced or rendered dysfunctional, potentially prejudicing Syria’s ability to mount a timely defense. Evidence gathering is impaired on all sides: documentary records may have been destroyed or rendered inaccessible, diminishing both the claimant’s capacity to prove its case and the State’s ability to produce responsive documents. Witness displacement, security risks, and travel restrictions affect both parties equally, necessitating reliance on remote testimony or written statements. These realities demand considerable tribunal flexibility while safeguarding both parties’ rights to equal treatment and a full opportunity to present their case.

Quantifying damages in claims against Syria is acutely difficult. Standard methodologies like Discounted Cash Flow (DCF), comparable transactions, and asset-based approaches require reliable market data, which armed conflict and economic isolation have rendered largely unavailable. Tribunals must address valuation date selection, conflict-zone risk premiums, and the absence of comparable transactions, often defaulting to cost-based or book-value methods.

Enforcement is similarly challenging. UNCITRAL awards under the New York Convention may be denied recognition on public policy grounds. ICSID awards, though subject to mandatory recognition under Article 54, remain exposed to sovereign immunity defenses under Article 55. Identifying commercial Syrian assets susceptible to execution is complicated by Syria’s limited foreign asset base and opaque state-owned enterprise structures. A successful award may thus prove difficult to monetize without voluntary compliance, a negotiated settlement, or a multi-jurisdictional enforcement campaign against State assets abroad.

Nevertheless, critical questions remain regarding the continuity of state obligations under the transitional government. Under the well-established principle that changes in government do not affect a State’s international legal obligations—rooted in the customary rule of pacta sunt servanda—Syria’s existing BITs, multilateral investment agreements, and ICSID Convention membership remain binding on the new authorities. However, while the March 2025 Constitutional Declaration affirms the State’s commitment to international treaties (Article 12), the transitional government faces persistent challenges regarding territorial control (although to a lesser extent since 2026) and institutional capacity—factors that may test the practical enforceability of these obligations and affect investor confidence in the nascent post-conflict government.

6. Conclusion and Recommendations

Syria’s existing BIT network consists predominantly of old-generation treaties with broad, unqualified protections and limited carve-outs—a framework increasingly at odds with modern investment treaty practice, which favors more precisely defined standards, transparency and anti-corruption mechanisms, environmental and social governance (ESG) standards, and sustainable development provisions—criteria increasingly demanded by contemporary investors and international financial institutions. Renegotiating these BITs to update standards of treatment and dispute resolution mechanisms along new-generation lines and drawing on contemporary treaty practice—including the UNCITRAL Reform Process, the EU’s Investment Court System proposals, and the latest ICSID Rule Amendments—would serve both State and investor interests by enhancing legal certainty and reducing exposure to overly expansive claims.

For example, in any modernization of Syria’s BIT network, the State should incorporate express general exceptions clauses. These could be modeled on Article 20 (XX) of the General Agreement on Tariffs and Trade (GATT) or on provisions found in recent-generation treaties, such as the 2012 US Model BIT and the investment chapter of the Comprehensive and Progressive Agreement for Trans-Pacific Partnership (CPTPP). Such clauses can carve out bona fide regulatory measures in areas such as public health, national security, environmental protection, and essential security interests from the scope of actionable treaty breaches.

In addition to ICSID and the other forums discussed above, Syria should consider accession to the Hague Conventions establishing the Permanent Court of Arbitration (PCA), to which it is not currently a contracting party.

Accession would send a powerful signal to the international investment community and could broaden and enhance the enforceability of arbitral awards by creating a more robust legal framework, increasing regional legitimacy, and providing a standardized, neutral, and reputable forum for dispute resolution. However, such accession, like ratification of new BITs, is constrained by the absence of a functioning parliament under the current transitional governance structure.

Early dispute management is important because it can reduce time and monetary costs, preserve commercial relationships, and prevent disagreements from escalating into formal disputes. This can be achieved through both institutional and procedural mechanisms.

Institutionally, the Syrian Investment Authority can serve as a single point of contact for investor grievances before they crystallize into formal treaty-based claims. More generally, transparent and predictable administrative procedures reduce the likelihood that regulatory measures will be characterized as arbitrary, discriminatory, or in breach of legitimate expectations under investment treaty standards. This may include advance notice of regulatory changes, meaningful public consultation, and reasoned decision-making.

Procedurally, Syria should consider introducing mandatory cooling-off periods and structured pre-arbitration consultation or mediation clauses in future BITs and investment contracts, requiring the exhaustion of good-faith negotiation and, where appropriate, mediation (e.g., under the ICSID Mediation Rules or the Singapore Convention on Mediation) before recourse to arbitration.

Complementary domestic legislative reform in Syria is also indispensable to translating treaty-level protections into tangible investor confidence on the ground. This may include clear land and property registration systems and anti-corruption legislation aligned with international standards. Engagement with multilateral institutions, such as the World Bank Group, the Multilateral Investment Guarantee Agency (MIGA), and UNCTAD, for technical assistance in legal reform, capacity building, and the provision of political risk insurance would further reinforce the credibility of Syria’s post-sanctions investment environment.

In the interim, building institutional capacity within Syria’s investor-facing authorities and the judiciary is essential to credibly administer and adjudicate investment disputes domestically. Two recent developments signal momentum. The Syrian Investment Authority created a dedicated international investment arbitration center in March 2026. A few months earlier, the Union of Chambers of Commerce of Syria established an international commercial arbitration center in November 2025. However, the neutrality, independence, efficiency, and fairness of these nascent domestic institutions remain untested.

The vast majority of regional and national arbitration centers worldwide are established by non-governmental entities, such as chambers of commerce, private associations, or other independent initiatives. Syria’s transitional government and its respective authorities should draw on this international experience and eventually delegate this mandate to non-government-affiliated stakeholders to guarantee the independence and impartiality of such institutions. In a post-war environment characterized by limited material and human resources, duplicative institutions may signal uncertainty rather than provide the guarantees and protections investors seek.

For investors, risk mitigation strategies—including political risk insurance, robust contractual protections with stabilization and arbitration clauses, and careful corporate structuring to ensure treaty coverage—remain indispensable tools for navigating the residual uncertainties of Syria’s evolving post-conflict investment environment.

Table A: Comparison of Bilateral Investment Treaty Standards of Treatment:

Wartime Applicability and Presence in Syria’s BIT Network

| Standard of Treatment | Wartime Applicability | Presence in Syria’s in-force BITs |

|---|---|---|

| Fair and Equitable Treatment (FET): Obliges the host state to act consistently, transparently, and in good faith, protecting the investor’s legitimate expectations. | Remains applicable, but tribunals may afford the State a wider margin of appreciation given wartime exigencies. | Virtually all of Syria’s in-force BITs are old-generation treaties that typically contain unqualified FET clauses. Confirmed in BITs with: Germany (1977), France (1977), Switzerland (2007), Türkiye (2004), Spain (2003), the Czech Republic (2008), Slovakia (2009), Romania (2008), Malaysia (2009), Azerbaijan (2009), Armenia (2009), Cyprus (2007), Greece (2003), the Philippines (2009), Lebanon (2010), Russia (2005), China (1996), Belarus (1998). |

| Full Protection and Security (FPS): Requires the host state to exercise due diligence in physically (and, on some readings, legally) protecting the investment. | Heightened relevance during armed conflict; directly engaged where assets are destroyed or left unprotected. However, the standard is one of due diligence, not strict liability. | Present in most European-model BITs and many others. Confirmed in BITs with: Germany (1977), France (1977), Switzerland (2007), Türkiye (2004), Spain (2003), the Czech Republic (2008), Slovakia (2009), Romania (2008), Malaysia (2009), Cyprus (2007), Greece (2003), Russia (2005), China (1996). |

| Protection Against Expropriation: Prohibits direct or indirect takings of an investment absent a public purpose, due process, non-discrimination, and prompt, adequate, and effective compensation. | Fully applicable; wartime seizures, requisitions, or legislative takings remain compensable under treaty law | Expropriation protection is the foundational provision of virtually every BIT worldwide; Syria’s BITs are no exception. All treaty partners’ BIT models include expropriation clauses, and Syrian domestic investment law itself references this protection. |

| National Treatment (NT): Requires the host state to treat foreign investors no less favorably than domestic investors in like circumstances. | Remains applicable, though comparator analysis may be complicated by conflict-related emergency measures of general application. | Standard provision in virtually all BIT models. Confirmed in BITs with: Germany (1977), France (1977), Switzerland (2007), Türkiye (2004), Spain (2003), the Czech Republic (2008), Slovakia (2009), Malaysia (2009), Cyprus (2007), Greece (2003), Russia (2005). |

| Most Favored Nation (MFN): Entitles investors to treatment no less favorable than that accorded to investors of any third state. | Continues to apply; no recognized wartime exception. | MFN is also one of the most ubiquitous BIT provisions. Confirmed in BITs with: Türkiye (2004) (Article III(2)) (The MFN clause in the Syria-Türkiye BIT was extensively litigated in Güriş v. Syria), Germany (1977), France (1977), Switzerland (2007), Spain (2003), the Czech Republic (2008), Slovakia (2009), Malaysia (2009), Cyprus (2007), Greece (2003), Russia (2005), China (1996). |

| Free Transfer of Funds: Guarantees the investor’s right to freely transfer profits, dividends, and capital out of the host state. | Applicable, but may be the standard most practically impaired during conflict due to sanctions regimes, banking disruptions, and currency controls. | Free transfer clauses are standard in virtually every BIT generation. Syrian domestic law also addresses repatriation rights. |

| Umbrella Clause: Elevates the host state’s contractual or other specific commitments to the investor to the level of treaty obligations. | Remains applicable; breach of state contracts during conflict may give rise to a treaty claim. | Umbrella clauses are characteristic of German, Swiss, and certain other European BIT models but are less common in Arab, Asian, and post-Soviet BIT models. Confirmed in BITs with: Germany (1977), France (1977), Switzerland (2007), the Czech Republic (2008), Romania (2008), Cyprus (2007), Greece (2003), Türkiye (2004) (See Güriş dissent noting use of MFN to import Umbrella Clause from Italy BIT). |