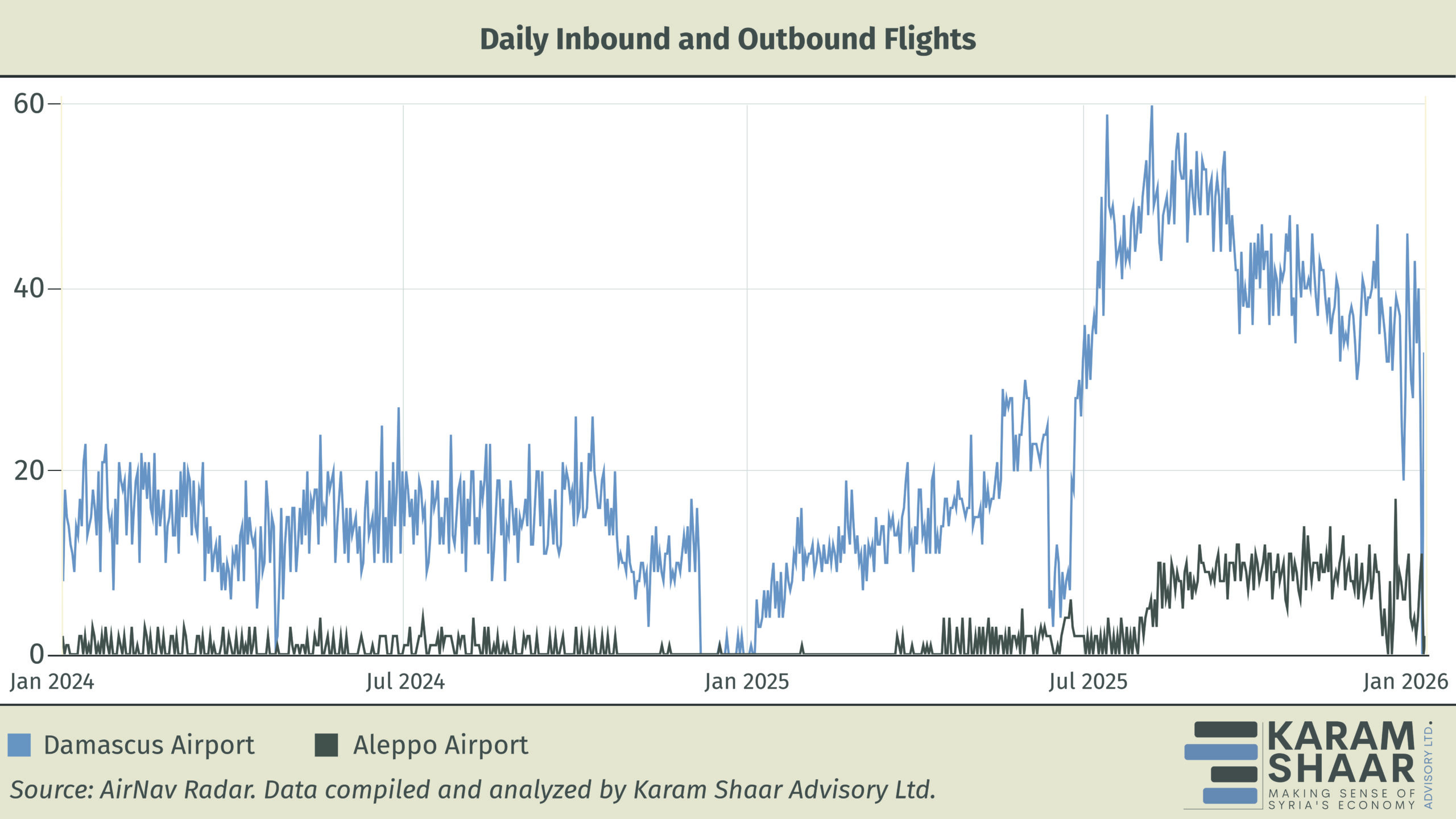

In 2025, Syria’s civil aviation sector recorded its highest level of activity since 2019, with the movement of more than 1.6 million passengers recorded across Damascus and Aleppo airports. Approximately 11,700 international flights operated—an increase of nearly 300 percent compared to 2024. Around 15 airlines also resumed regular operations during the year.

A marked acceleration occurred in the second half of 2025 following the easing of most US sanctions on 30 June. Based on AirNav Radar, average daily movements across Damascus and Aleppo airports increased from approximately 15 flights per day during the first half of the year to nearly 49 flights per day thereafter. The timing suggests that easing sanctions facilitated the rebound, particularly by encouraging operational normalization.

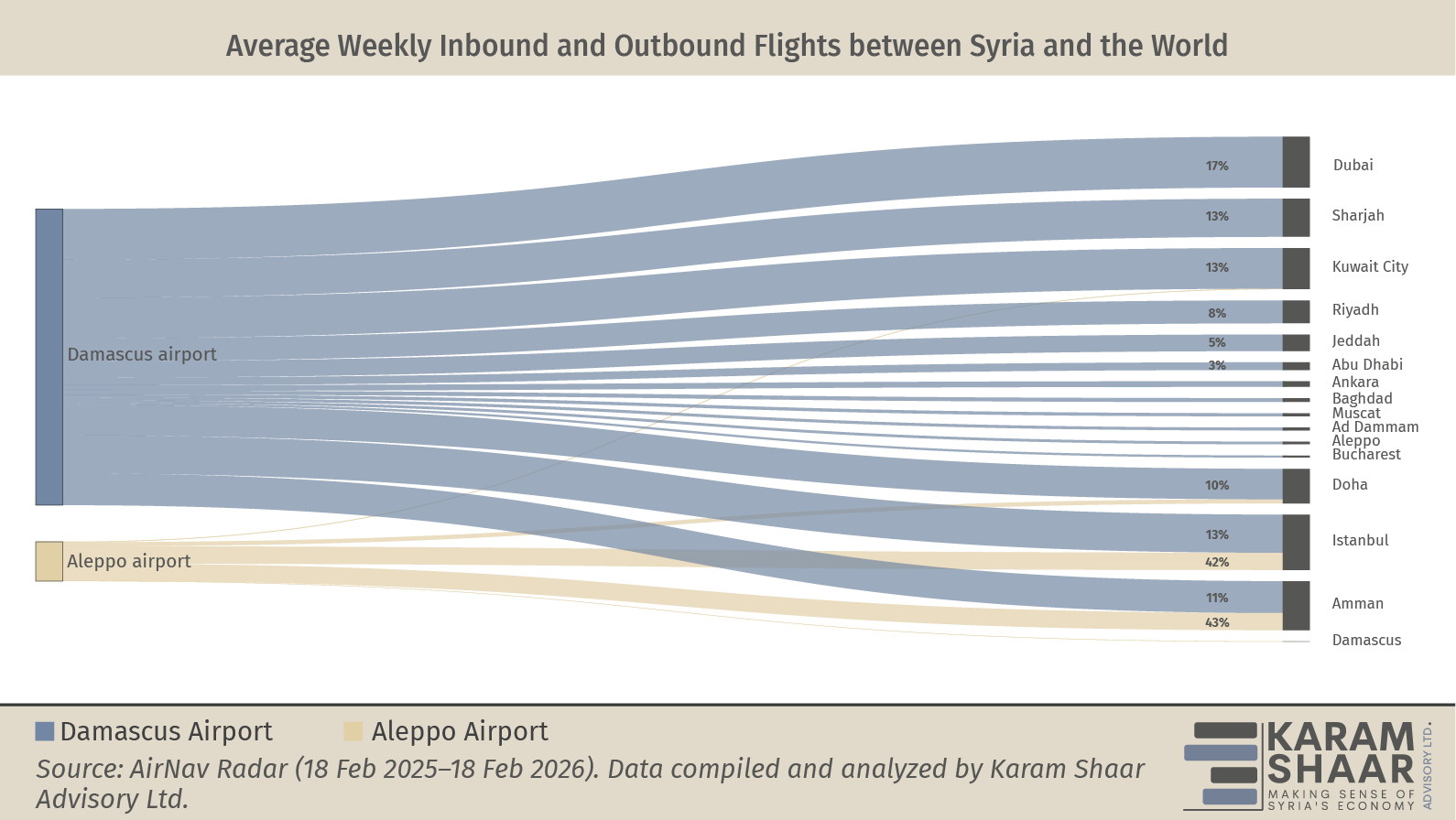

Domestic carriers operated approximately 57 percent of total flights in 2025—a comparatively high share relative to neighboring markets, where national airlines accounted for around 36 percent of traffic in Iraq and 46 percent in Lebanon. Traffic remained heavily concentrated within a narrow regional network. Four Gulf destinations served through Damascus—Dubai (16.7 percent), Kuwait (13.3 percent), Sharjah (12.6 percent), and Doha (10.1 percent)—collectively accounted for more than half of all trips. Meanwhile, roughly 84 percent of traffic through Aleppo International Airport was directed exclusively toward Türkiye and Jordan. These traffic distribution figures are based on ADS-B data sourced from AirNav Radar and analyzed by Karam Shaar Advisory.

By the end of 2025, direct connectivity with Europe remained limited. Aside from two weekly flights to Bucharest, there was no effective return of major European or global carriers and no corresponding expansion of the national carrier into broader international airspace. Against this backdrop, the analysis examines the regulatory and operational constraints that have kept the recovery largely confined.

Domestic Operational Capacity

Beyond security risks, entry into Syria’s aviation market remains inhibited by inadequate operational standards at Syrian airports. International standards for airport regulation and operations, as defined by the International Civil Aviation Organization (ICAO), encompass instrument landing systems (ILS), radar and communication equipment, aircraft rescue and firefighting services (RFFS), operational manuals, certification procedures, and ongoing regulatory oversight. In Syria, gaps in several of these areas have constrained full operational normalization.

Over the past years, Syria’s aviation sector has experienced significant deterioration in technical and regulatory capacity. Sanctions regimes imposed by the European Union and the United States restricted access to dual-use aviation technologies and specialized equipment.

In this context, essential systems and equipment support provided by Türkiye to Damascus International Airport preceded the entry of Turkish carriers into the market, underscoring the importance of easing operational barriers to facilitate market entry. In early 2026, a new civil radar system entered into service at Damascus International Airport, representing a further step toward improving air traffic management. While these measures indicate incremental improvements, they do not yet amount to full operational normalization.