After fourteen years of conflict and crippling international sanctions, Syria’s banking and financial sectors are on the brink. The fall of the Assad regime has not yet brought relief; instead, it has exposed new layers of fragility.

In February 2025, the Central Bank of Syria (CBS) imposed strict limits on cash withdrawals. Customers could take out only SYP 200,000 (around USD 20) per transaction per week, a limit raised to SYP 600,000 (around USD 60) in early August. On 14 August, the Commercial Bank of Syria (CBoS) also raised the daily withdrawal ceiling at in-branch POS machines to SYP 1 million (around USD 100.4). These measures effectively froze deposits, leaving families unable to meet daily needs and businesses unable to cover operating costs—even as banks continued to show substantial cash holdings on paper.

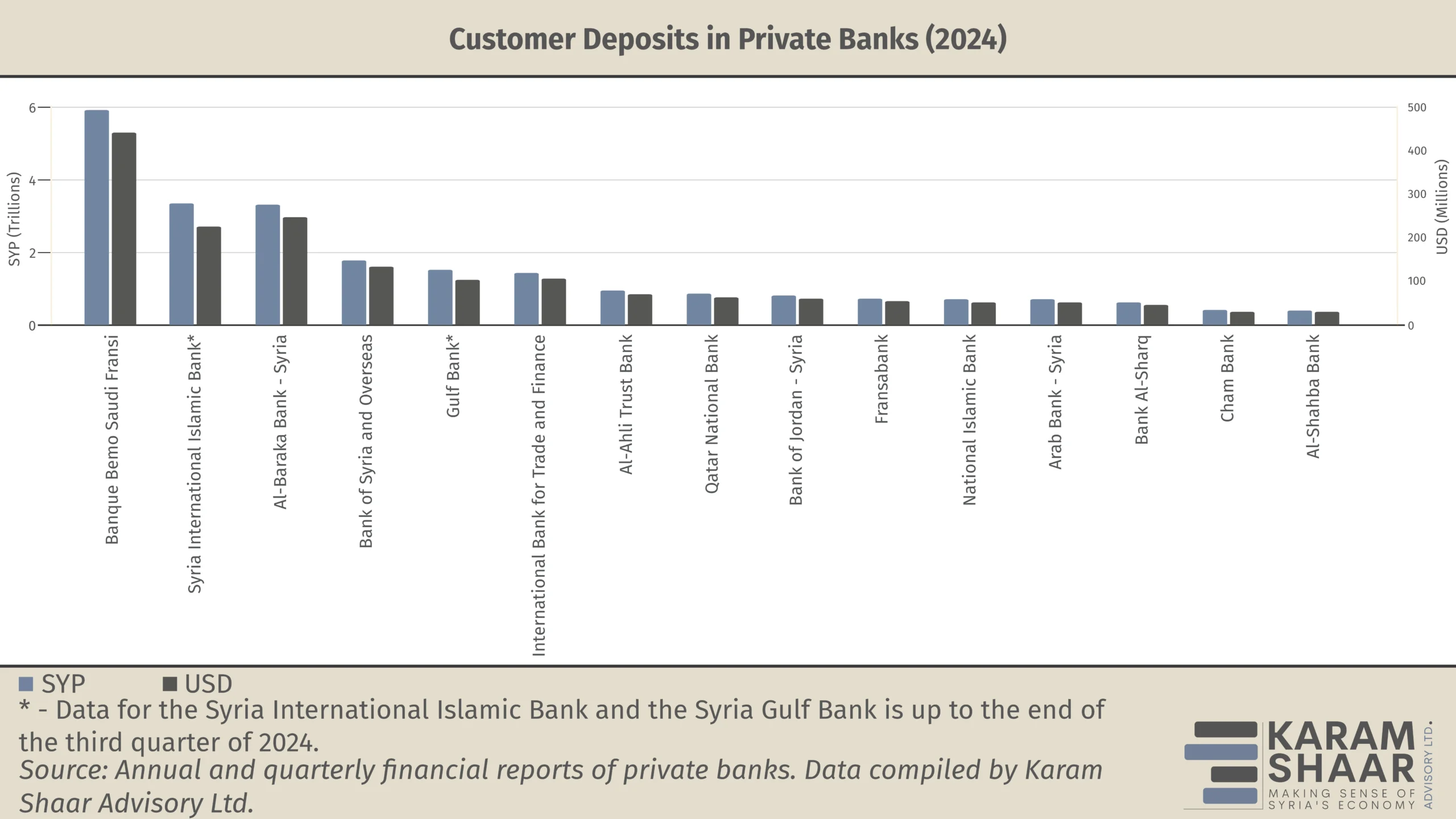

By the end of 2024, customer deposits in private banks (in SYP and their foreign-currency equivalent) stood at SYP 23.5 trillion (USD 1.7 billion), based on annual financial reports reviewed by the authors. For public banks, the latest data from the Central Bureau of Statistics show that customer deposits at the CBoS reached SYP 2.6 trillion (USD 151.5 million) at the end of 2022, compared with SYP 5.6 trillion (USD 326.5 million) for private banks in the same year.

Yet most of this money sits with the CBS, which withholds liquidity from commercial banks—rendering deposits inaccessible. The CBS never clarified its reasons, leaving these funds effectively frozen. In bilateral discussions with the authors, Syrian authorities and bankers acknowledged that the CBS did not have enough liquidity in its vaults to meet demand. In a recent interview, Central Bank Governor AbdulKader Husrieh mentioned the “lack of domestic liquidity” as a significant challenge facing the economy today.

Whatever the motive, the restrictions created what became known as the “bank balance market,” where desperate depositors sell semi-frozen balances at steep discounts to traders with liquidity, who then profit by securing exemptions or withdrawing funds gradually. Such secondary markets for deposits are not unique to Syria. They have appeared in several crisis-hit economies where banks impose withdrawal limits, giving rise to the phenomenon of deposit “haircuts.”

For instance, in Lebanon during the 2019 financial crisis, the “Lebanese dollar” or “lollar” emerged after banks imposed de facto capital controls. Depositors were forced to either leave their funds trapped in accounts or to withdraw them at deeply discounted rates, far below the market rate. Similarly, Argentina in 2001–2002 imposed the “corralito,” forcibly converting USD deposits into pesos at 1.4 ARS/USD while the black-market rate neared 4 ARS/USD. Households and firms were forced to take heavy losses to access their own cash.