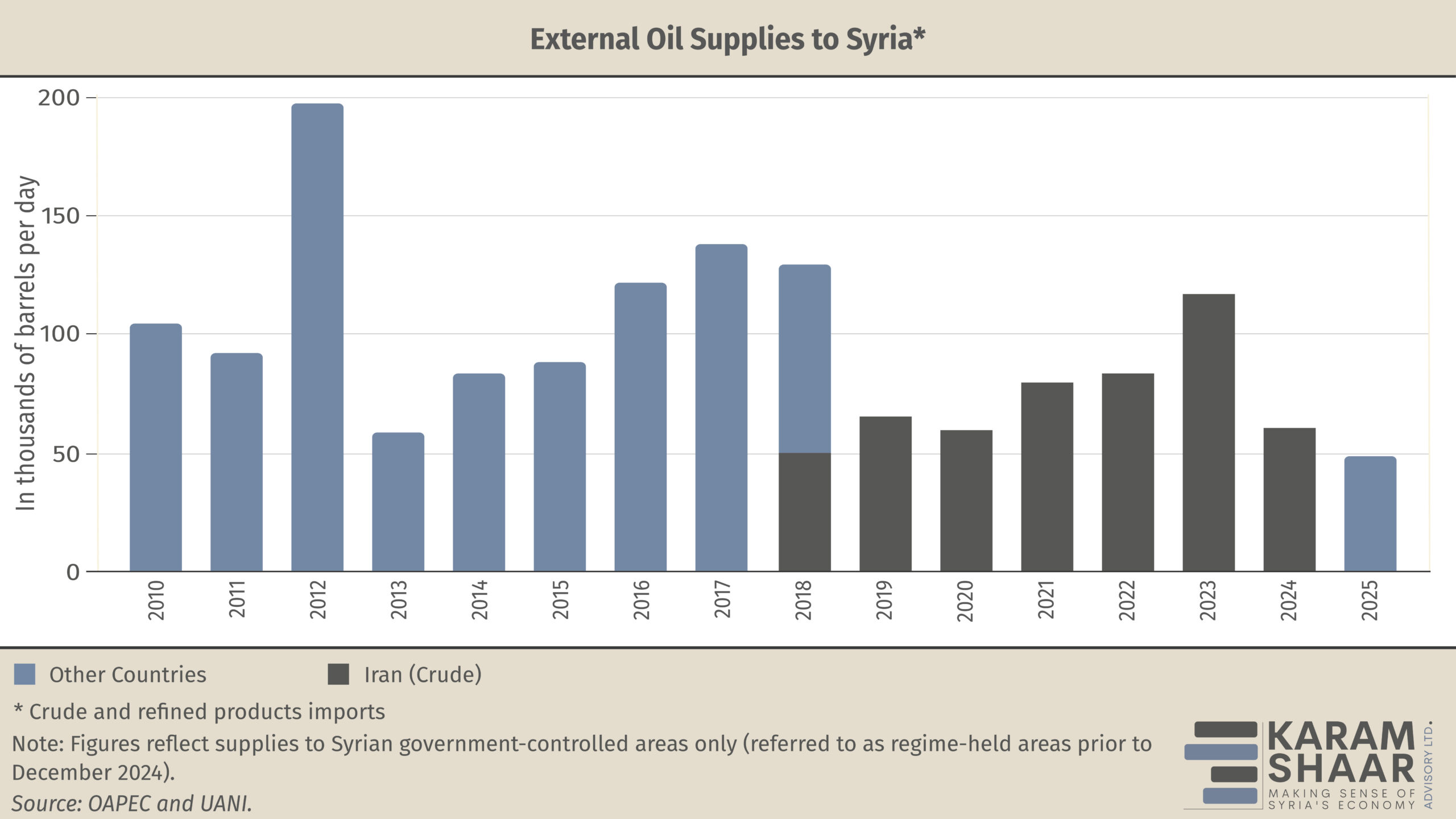

On the eve of the Assad regime’s collapse in December 2024, an Iranian oil tanker bound for Syria made a U-turn in the Red Sea. Once an oil exporter producing around 150,000 barrels per day (bpd) in 2010, Syria had, during the conflict, become dependent on Iranian oil imports. Between 2011 and 2024, Iran reportedly provided approximately USD 14 billion worth of oil and petroleum derivatives, averaging about 78,500 bpd during the final five years of Assad’s rule. These supplies were financed through credit lines. Assad’s fall caused the immediate collapse of this oil-supply arrangement, resulting in an acute shortage and forcing Syria to seek alternative sources of oil supply.

The Caretaker Government—formed after the regime’s fall—responded to the crisis and, on 20 January 2025, announced several tenders for importing 4.2 million barrels of crude oil and approximately 2.8 million barrels of refined products. All tenders attracted no or only negligible responses, as major suppliers remained hesitant to enter payment arrangements with the new Syrian authorities, particularly given the continued presence of sanctions at the time.

Reports indicated that, at the beginning of January, the Iraqi government resumed oil supplies under a mechanism in place since the previous regime era, estimated at around 33,000 bpd, following signals from the US and Türkiye emphasizing its importance in supporting the new Syrian administration. The new quantities were not disclosed, and no further information was provided on whether these imports remain active. This ambiguity was reinforced after the Iraqi Ministry of Oil denied the existence of such supplies altogether, although it remains unclear whether this denial was intended to shield Iraq from potential sanctions.

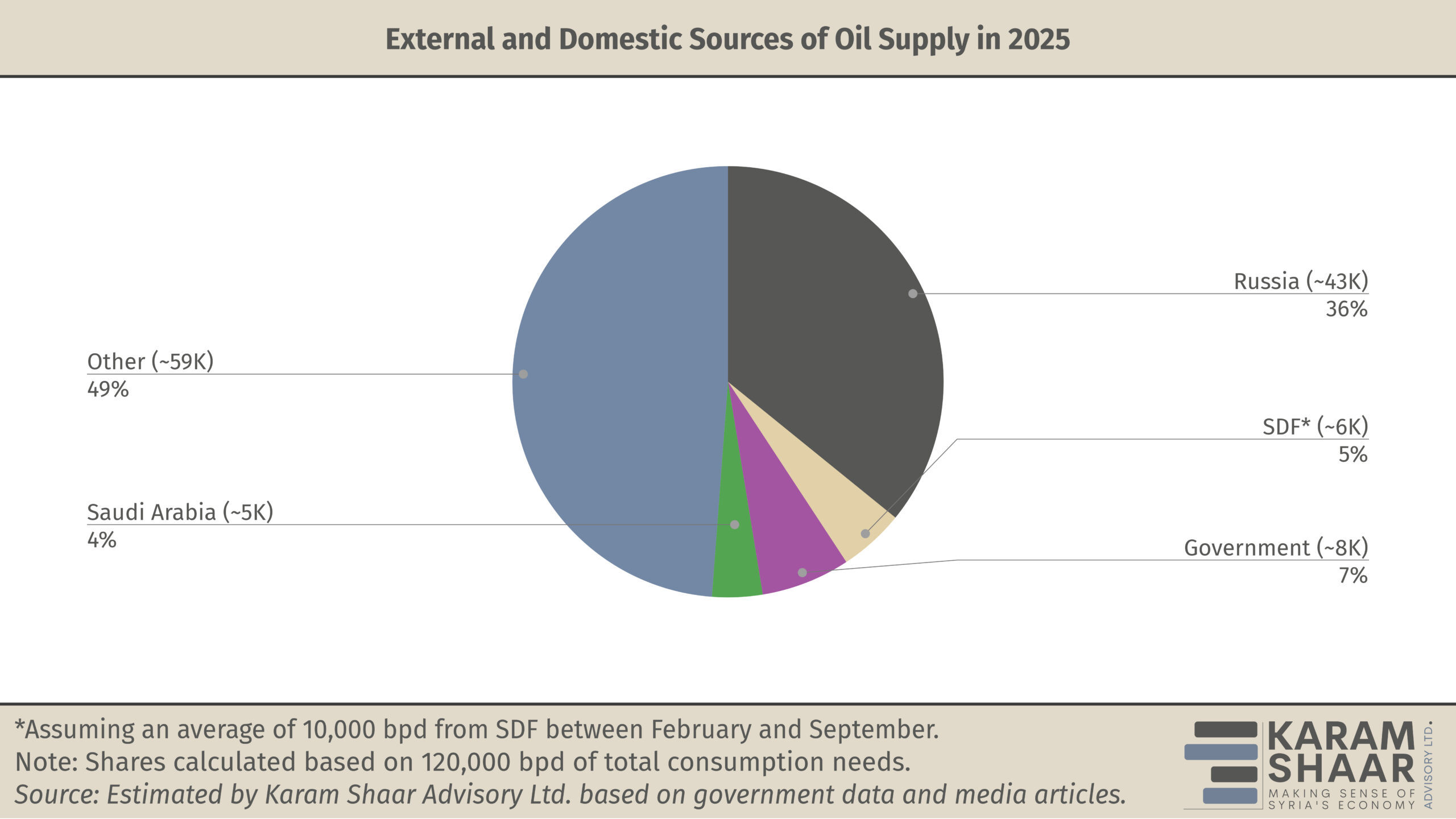

Seeking to secure short-term domestic oil supplies, the government concluded an urgent agreement with the Syrian Democratic Forces (SDF) in late February 2025. Sources differed on the quantities to be supplied from the fields in Al-Hasakah and Deir Ezzor to government-held areas, but estimates ranged between 5,000 and 15,000 bpd. The three-month arrangement was renewed in June 2025.

Meanwhile, as sanctions began to ease, the authorities announced additional tenders in March 2025 to procure 7 million barrels of light crude. The same tender was reannounced in June, apparently because the earlier round received no positive responses. The Ministry of Energy likewise announced no results for that tender, indicating that no offers were received. The most recent tender, announced in November, is a further repetition of the previous ones; however, Youssef Qabalaoui, CEO of the Syrian Petroleum Company, revealed that the tender was awarded to a company without disclosing its name.

These volumes were clearly insufficient to close the domestic demand gap. Syria subsequently turned to Russia to source oil, with the first shipment reported to have arrived in early March. By the end of October 2025, Russia had sent 17 shipments totaling more than 15.7 million barrels. We have found no evidence of Russian supplies through November and December.

Russia became Syria’s dominant external oil supplier following the Iranian cutoff, delivering approximately 58,000 bpd of crude oil between March and October 2025. Saudi Arabia, in turn, granted 1.65 million barrels of light crude in November as part of efforts to support the Syrian government’s economic recovery. With the arrival of Saudi oil, Syria gained an additional 27,500 bpd, sufficient through the end of the year, according to Qabalaoui.

Separately, the government controls several oil fields in the west Euphrates and the Badia, producing approximately 8,000 bpd, according to the Minister of Energy, who revealed that total consumption needs are estimated at 120,000 bpd.