In the previous issue of Syria in Figures, analysis of the Syrian pound’s exchange-rate movements in 2025 showed that sharp swings were driven less by economic fundamentals than by market reactions to political and economic announcements. The currency’s broader trend, however, continued to point to gradual depreciation, reflecting a structural shortage of foreign currency.

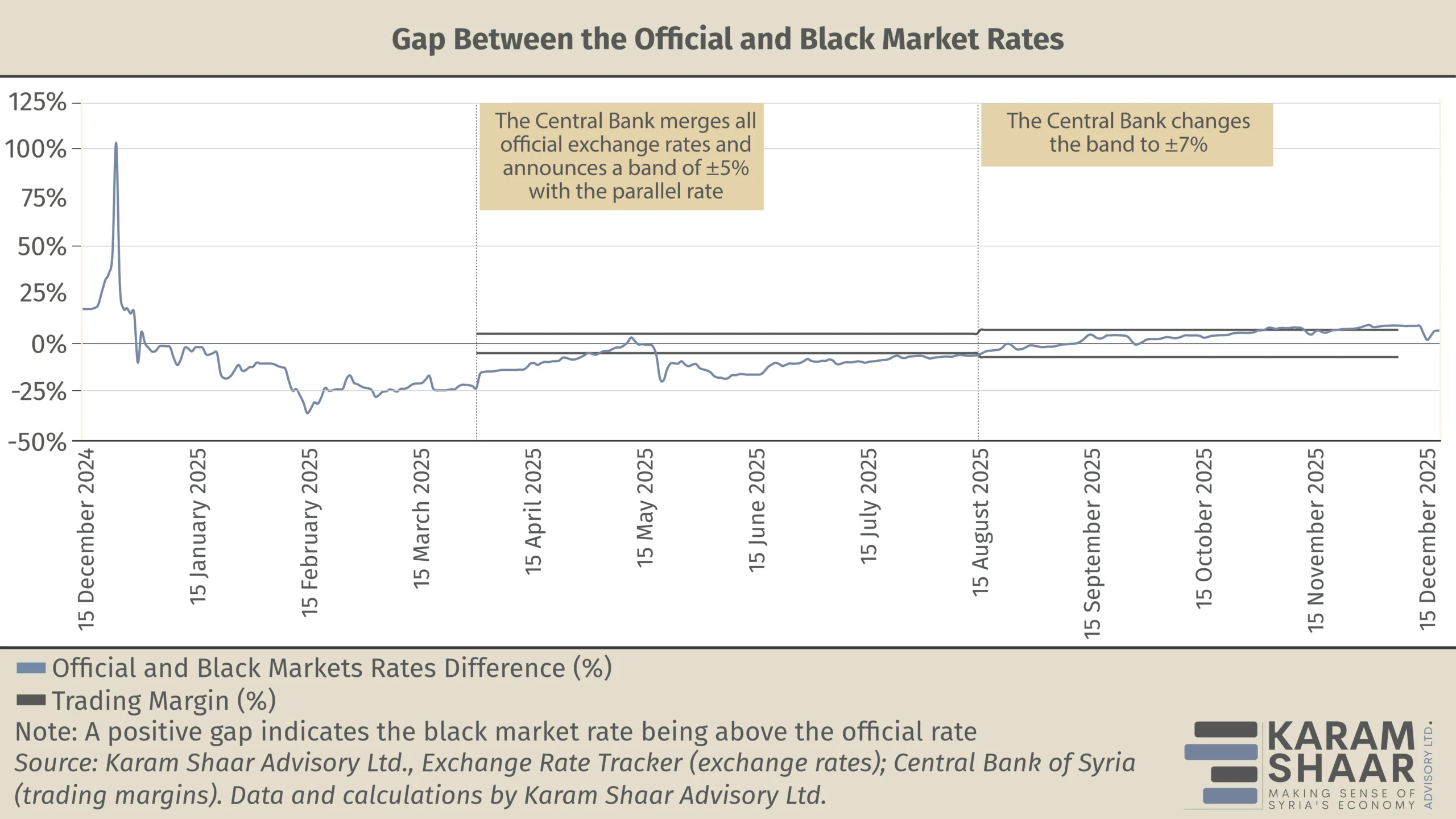

The existence of two de facto exchange rates, official and black-market, continues to distort economic activity that must use both across different transactions. At its peak on 5 February 2025, the gap between the two exceeded 35 percent, complicating accounting and financial planning, weakening investor confidence, and delaying long-term investment decisions.

Monetary Policy Actions

Following post-war volatility, the Central Bank of Syria made its first formal attempt to manage the exchange rate. On 23 March 2025, it announced the unification of its exchange-rate bulletins and mandated a ±5 percent pricing band for licensed banks and exchange companies. The aim was to narrow the gap between the official and black-market rates while allowing limited flexibility for formal market participants.

Although the measure appeared technically straightforward, its limits quickly became clear. Between 23 March and 5 August, the black-market rate remained outside the designated band on 120 of 136 trading days, nearly 88 percent of the period, based on our analysis of Syrian pound exchange-rate data.

On 6 August, the band was expanded to ±7 percent, implicitly acknowledging the earlier framework’s shortcomings. The exchange rate remained within the new corridor until 27 October, when it first breached the limit. From 27 October to 14 December, the gap again exceeded the ±7 percent threshold on 34 of 54 days. While the wider band initially restrained movements, it ultimately failed to anchor market expectations, eroding the credibility of the Central Bank’s framework.