Amid high expectations for the role of Syrian banks in the reconstruction phase, the country’s private banking sector faces a binding capital constraint. Total private banking capital (equity), based on our analysis of banks’ financial statements published on the Damascus Securities Exchange website, remains below 1 billion USD, limiting banks’ capacity to withstand financial shocks, finance imports, and extend credit. Against this backdrop, recapitalization emerges as a central pillar of efforts to reform the banking sector.

This article reviews the balance sheets of private Syrian banks as published on the Exchange website, examines the composition and distribution of assets and capital domestically and abroad, assesses how this distribution affects banks’ capacity to finance, and outlines potential recapitalization pathways.

All Syrian private banks combined hold equity equal to that of a single regional bank

As of Q4 2025, the total equity of all Syrian private banks stood at SYP (old) 8.7 trillion (about USD 795 million). This is roughly equivalent to the equity of a single bank in Jordan, Egypt, or Tunisia, ranking in the lowest quartile among the largest 100 Arab banks.

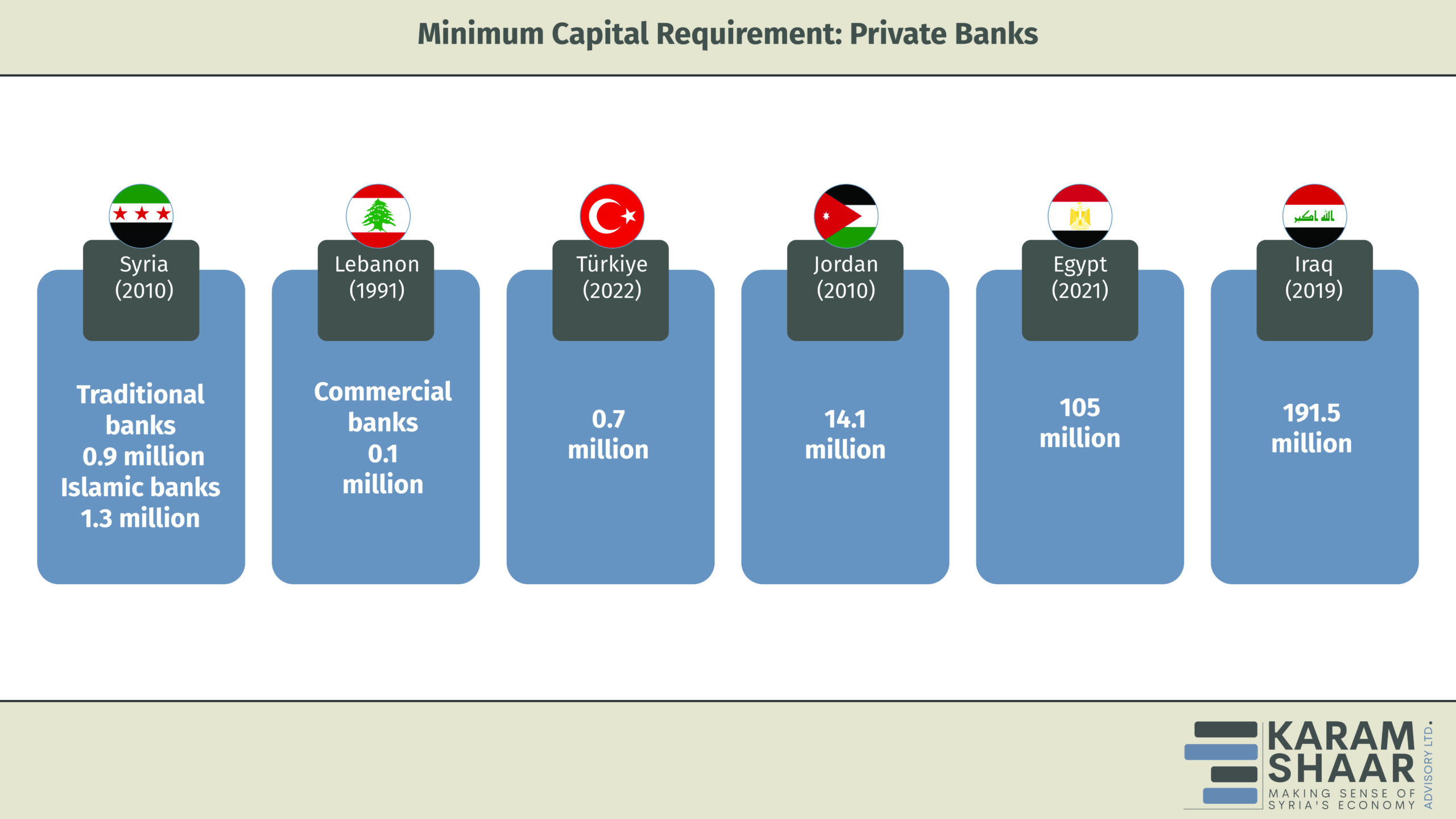

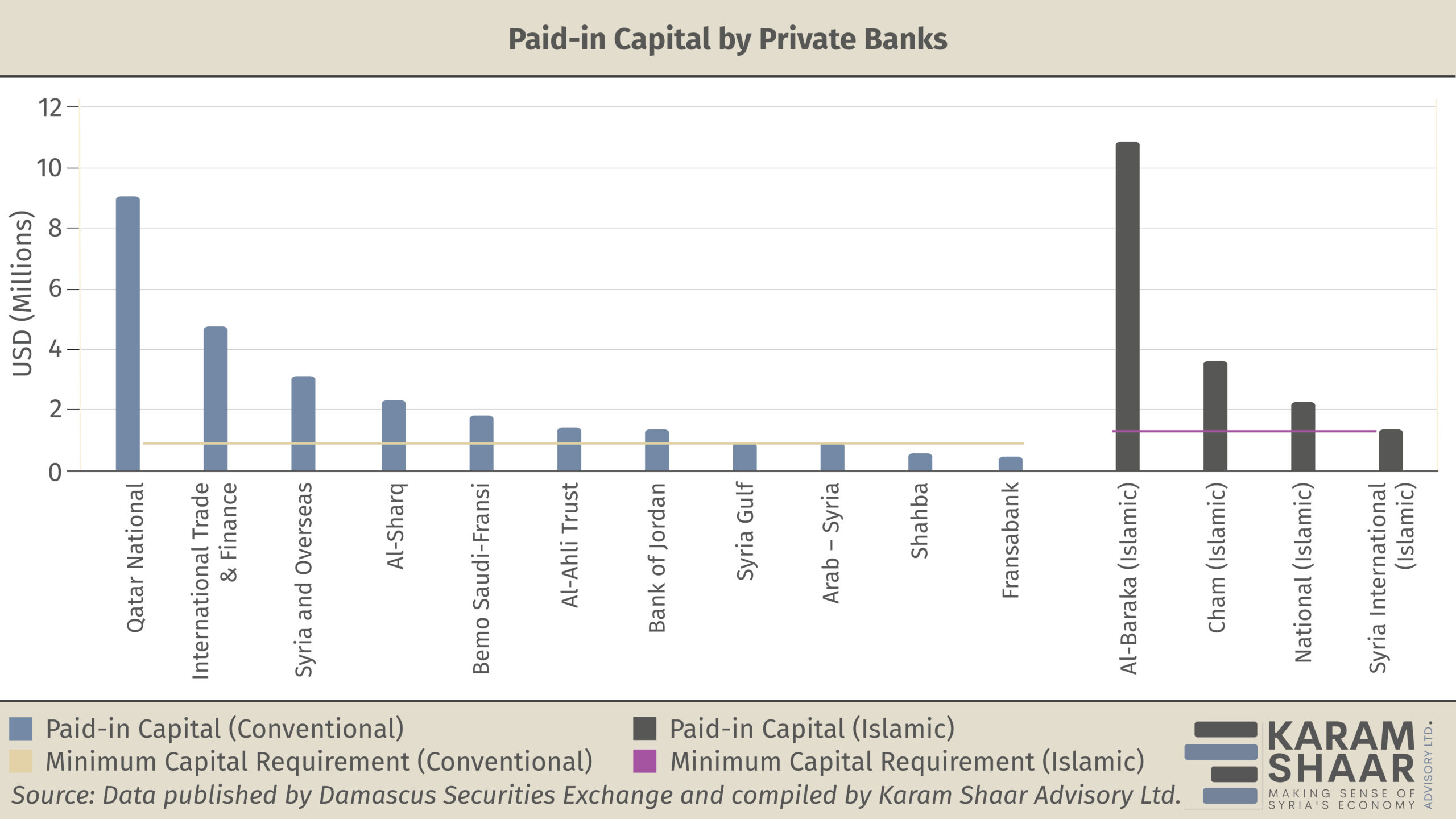

Despite this limited aggregate capital base, most banks formally comply with domestic regulatory capital requirements. Syrian legislation sets the minimum capital requirement (MCR) at SYP (old) 10 billion (USD 0.9 million) for conventional banks and SYP (old) 15 billion (USD 1.3 million) for Islamic banks. Most private banks meet or exceed these thresholds, with some holding paid-in capital several times the required minimum.

In 2010, when the exchange rate stood at SYP 47 per USD, the MCR was equivalent to USD 212.7 million for conventional banks and USD 319.1 million for Islamic banks—levels broadly aligned with neighboring countries at the time. Since then, however, the requirement has not been adjusted. As inflation and currency depreciation accelerated during the conflict, the inflation-adjusted value of the MCR declined sharply.

As a result, Syria’s MCR is now only a fraction of its pre-war USD equivalent and remains exceptionally low compared with regional peers (excluding Lebanon, which is undergoing a severe banking crisis).

Capital Adequacy: Compliance with Obsolete Standards

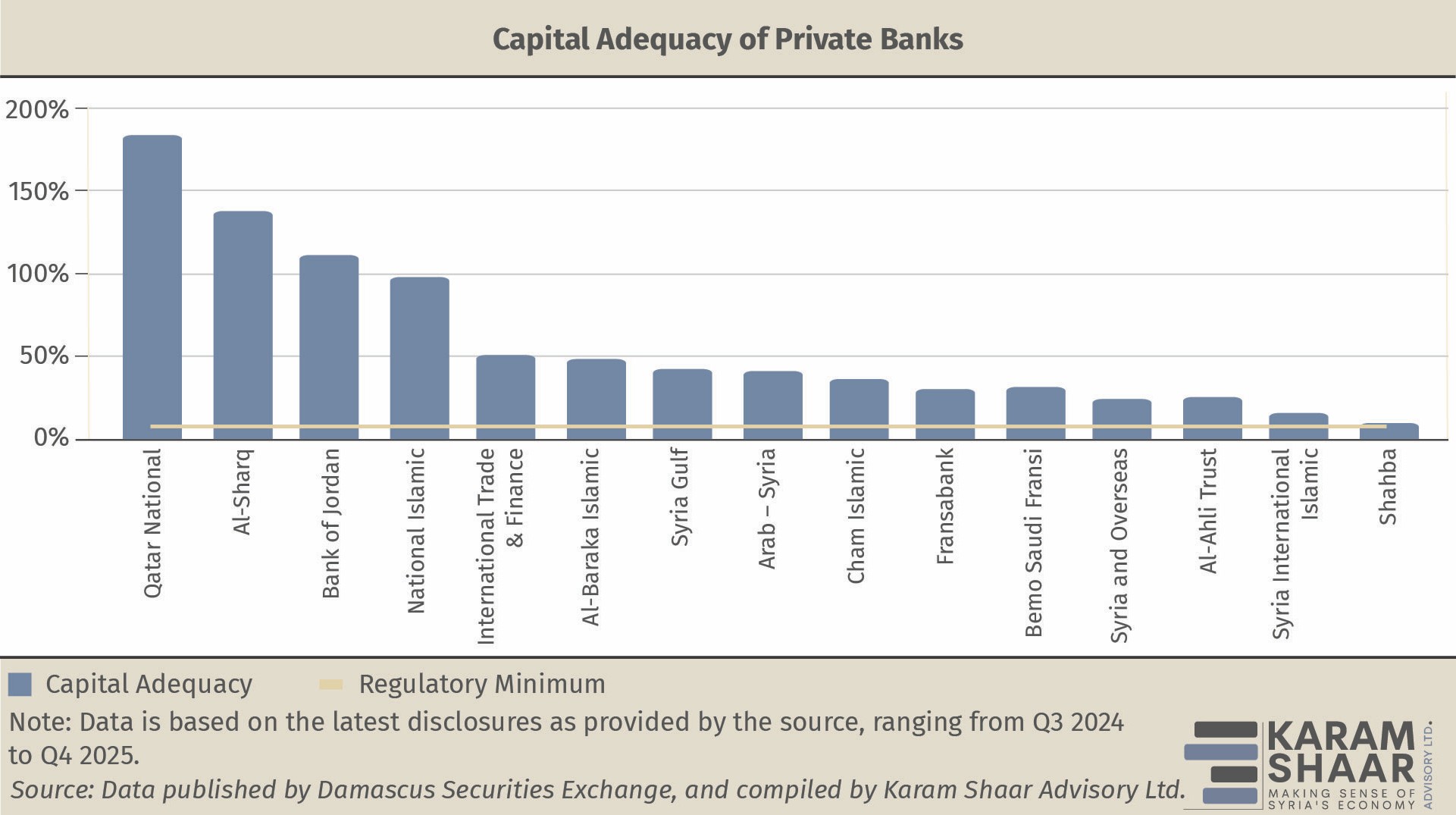

At first glance, Syrian private banks appear exceptionally well capitalized. As of Q4 2025, our calculations show that their capital adequacy ratios (CARs) far exceeded the Central Bank’s regulatory minimum of 8 percent as well as the Basel III Committee’s 10.5 percent requirement, and for three banks, exceeded 100 percent. Compared with leading international institutions, Syrian banks seem even stronger on this metric: CARs stand at about 50 percent for some major Gulf banks and approximately 17 percent for major US banks such as JP Morgan and Citibank.

These elevated ratios, however, largely reflect restrictive lending (the denominator) rather than capital depth (the numerator), mechanically inflating the ratio without a corresponding expansion in high-quality capital. As of Q3 2025, net credit facilities account for only 12.3 percent of total assets across Syrian private banks—the asset class most exposed to credit risk and a central determinant in CAR calculations.

Another important factor to highlight is Syria’s continued application of Basel II standards, whereas Basel III imposes stricter capital quality requirements, resulting in materially lower effective capital adequacy ratios under comparable balance-sheet conditions.

Balances and deposits abroad at the expense of domestic lending

During the conflict, Syrian private banks increased their balances and deposits with foreign banks—primarily with their parent banking groups—while reducing exposure to domestic credit risk. This shift reflected a deliberate tightening of local lending policies.

According to our calculations, the average ratio of capital held in foreign accounts to total domestic credit is 7.2. In practical terms, for every SYP extended in domestic lending, more than SYP 7 is held in foreign accounts. This allocation significantly constrains the expansion of domestic credit, compounded by the Central Bank’s liquidity constraints since 2019–2020.

The problem is exacerbated by limited recoverability in some cases, particularly for banks affiliated with Lebanese banking groups, and by other banks’ reluctance to repatriate funds in line with their internal risk policies.

This dynamic raises questions about the effectiveness of prudential oversight and the Central Bank’s role in aligning asset allocation practices with broader financial stability and growth objectives.

The role of local contribution in capitalization

Foreign ownership limits constrain the scope for recapitalization through external investors alone, making stronger local participation unavoidable.

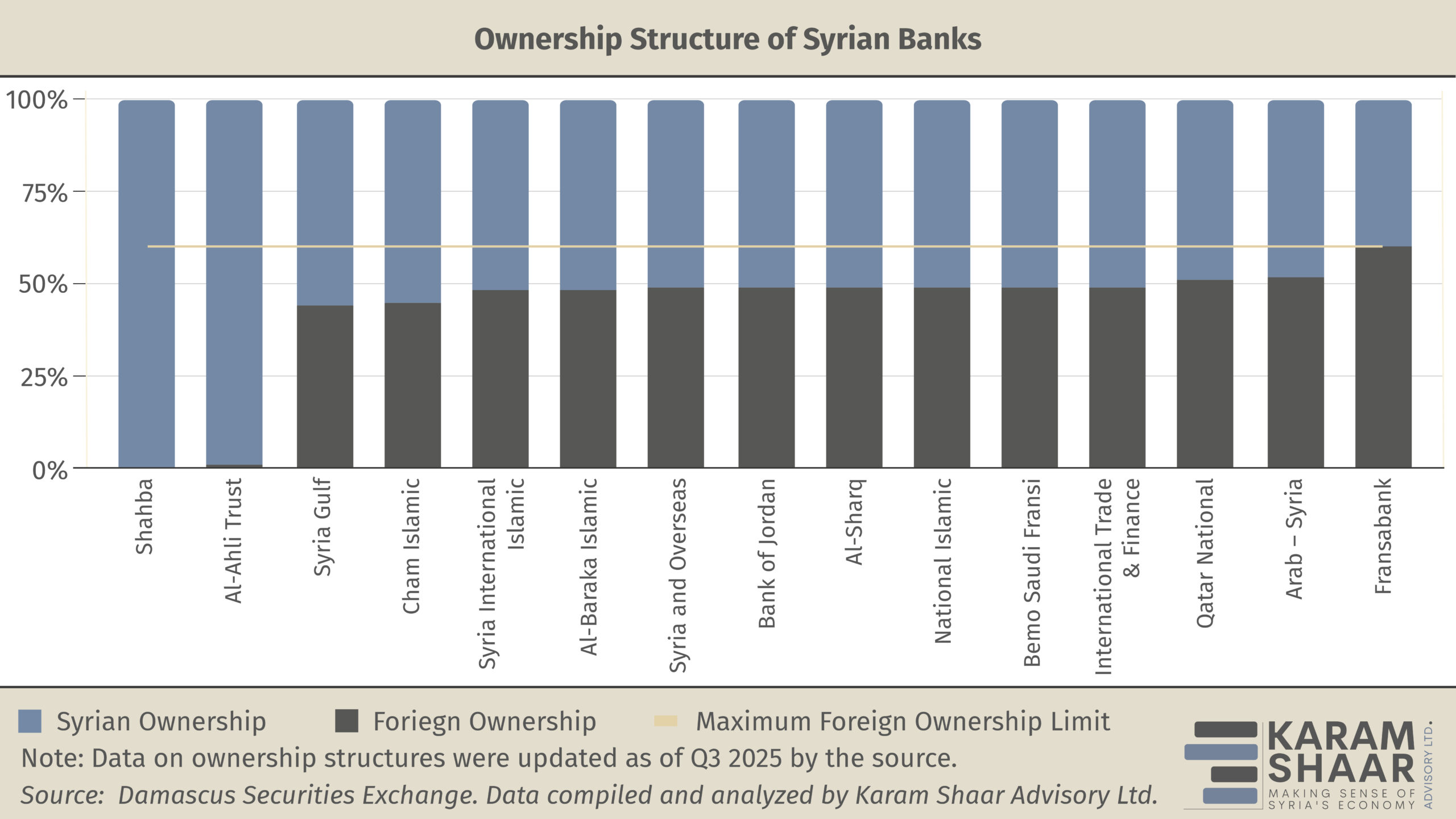

Under Syrian legislation, the maximum share limit for non-Syrian owners is 49 percent, which rises to 60 percent if the parent banking group abroad holds the largest share. Except for Al-Ahli Trust Ahli Bank and Shahba Bank, which are fully Syrian-owned, most banks’ foreign ownership ranges between 44 percent and 60 percent, mostly held by the strategic partner. This leaves limited headroom for meaningful capital increases through foreign participation alone.

By contrast, there are no statutory limits on local ownership. Shares are distributed among Syrian individuals, legal entities, and the public sector, which holds 5.2 percent of private banks’ total capital. Because foreign ownership is capped, any recapitalization strategy must mobilize domestic capital alongside foreign participation.

Given these constraints, recapitalization should begin with regulatory action. The Central Bank should raise the minimum capital requirement to offset the SYP’s depreciation during the conflict and set a clear, sufficient compliance deadline that takes into account the struggles faced by those banks.

Regarding foreign ownership, authorities could consult parent banking groups to cover their proportional share of any capital increase or facilitate the sale of shares to interested foreign investors. An acquisition request was recently announced by Estithmar Holding to acquire a majority stake in Shahba Bank and a 30 percent stake in Syrian International Islamic Bank, subject to regulatory approval.

On the domestic side, several mechanisms are available. Banks could capitalize retained earnings by distributing bonus shares rather than cash dividends. Large depositors could be offered incentives to convert long-term deposits into equity instruments, easing liquidity pressures while strengthening capital buffers. The government could also increase the participation of public entities, including the Syrian Sovereign Fund and the Syrian Development Fund, with provision for eventual resale to founding shareholders.

Ultimately, the success of any recapitalization strategy depends on coordinated action among regulators, the government, bank management, and depositors within a transparent framework focused on financial stability.