Building on our previous article on Syria’s gas pipeline network, oil pipelines form the backbone of the country’s petroleum sector. Before 2011, Syria was a net oil producer, with pipelines enabling crude exports through Mediterranean ports. It also served as a transit corridor for Saudi (1950–1990) and Iraqi (1952–2003) oil bound for international markets. This article reviews Syria’s domestic and regional oil networks and recent efforts to restore cross-border routes.

Years of armed conflict have inflicted catastrophic damage on this infrastructure and fragmented control over critical networks. More than 1,000 km of oil and gas pipelines in northeastern Syria alone are now estimated to require complete replacement rather than repair. This assessment was echoed by Youssef Qabalawi, CEO of the Syrian Petroleum Company, who stated that the nationwide pipeline network is severely deteriorated, lacks maintenance, and contains chemical deposits and salts.

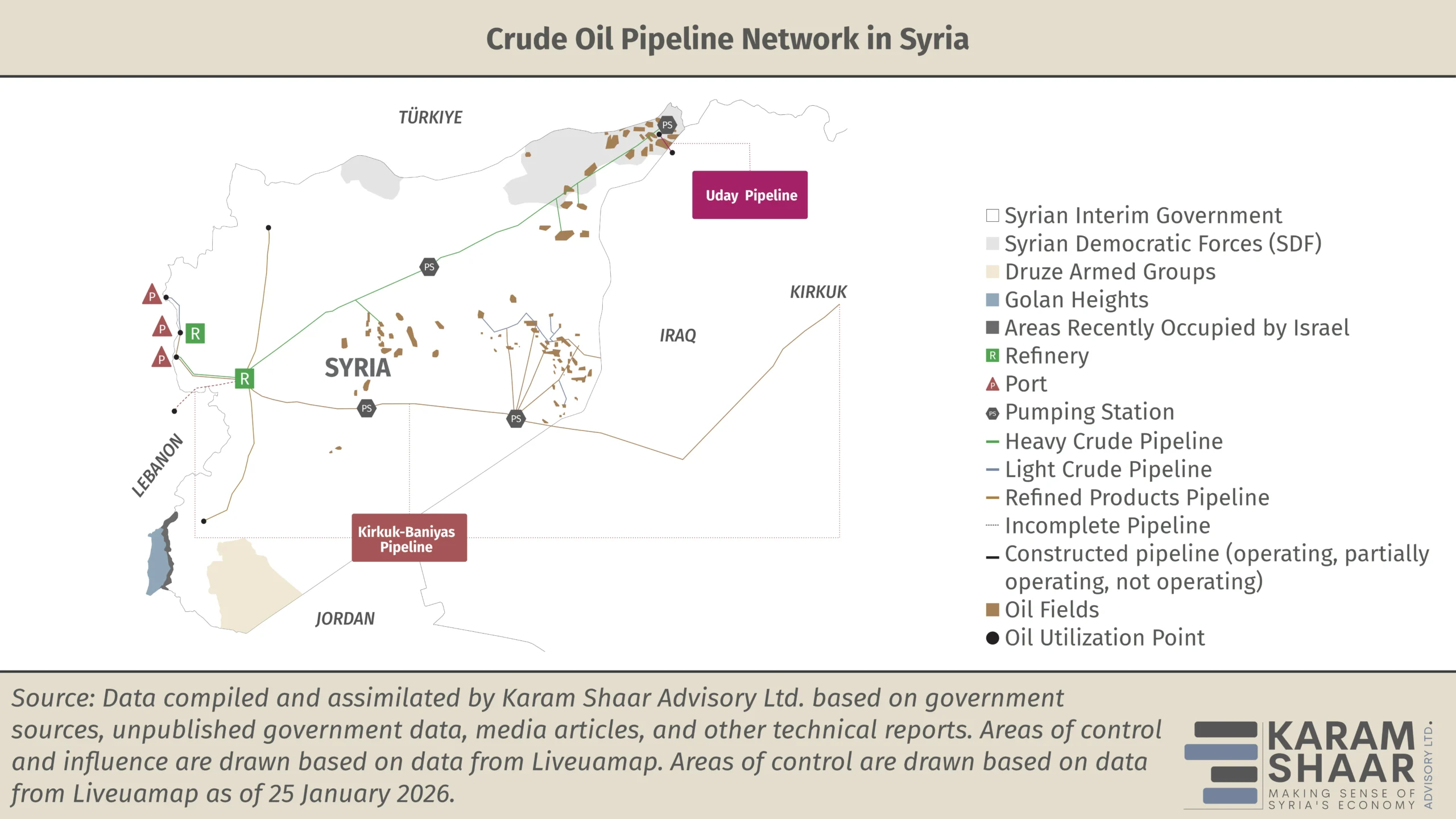

Syria’s domestic oil pipeline system, developed primarily in the late 20th century, connects scattered production fields across the country’s eastern and central regions to the Homs and Baniyas refineries and supports exports through the Baniyas and Tartous offshore terminals.

The heavy oil system runs from Tal Adas in the Rumeilan fields to Tartous, stretching about 663 km and designed for a capacity of 300 thousand barrels per day (bpd). The light oil system links Deir Ezzor to Baniyas across a total network of about 2,000 km, of which 1,185 km were operational before the conflict. Four main gas-turbine pumping stations operate on the light crude system, while nine electrically powered stations serve the heavy crude system. Years of conflict have left much of this infrastructure destroyed.

Syria’s oil production stood at 387,000 bpd in 2010, of which about 40 percent was exported mainly to Europe. Years of conflict and sanctions eliminated exports, though fragmentation later allowed Kurdish-controlled areas to trade with Iraqi Kurdistan through the “Uday” pipeline.

A previous Syria in Figures article on oil supplies in 2025 showed that government-controlled areas now rely almost entirely on imports. This has pushed Damascus to seek more stable and cost-efficient means of supply, including pipelines, where Syria is currently looking for opportunities. Historically, Syria’s Mediterranean terminals positioned it as a transit corridor, with two major lines crossing its territory: the Trans-Arabian pipeline (Tapline) and the Kirkuk-Baniyas pipeline, both now dormant or abandoned.

The Kirkuk-Baniyas pipeline, completed in 1952, is Syria’s most important transit asset, linking Iraq’s Kirkuk fields to the port of Baniyas. The 800 km line, with a capacity of 300,000 bpd, was suspended in 1956–1957 during the Suez crisis, again from 1982 to 2000 when Syria sided with Iran during the Iran–Iraq War, and finally in 2003 following the US invasion of Iraq and sabotage that rendered it inoperative, leaving it dormant for more than two decades.

During this period, efforts to revive the pipeline intermittently resumed. In 2007, Stroytransgaz, a major Russian oil infrastructure firm, opened discussions with Iraqi authorities, though planned repairs were postponed in 2009. Reports later suggested the US was opposing the project to increase economic pressure on Damascus. In 2010, Syrian and Iraqi authorities signed an agreement to build two new Kirkuk-Baniyas pipelines, one for light crude (1.25 million bpd) and one for heavier crude (1.5 million bpd). A year later, both sides met again to discuss restoring the original single line.

The pipeline fell off the agenda during the early years of the conflict. In mid-2019, however, news reported that Iran had revived a proposal for alternative export routes, either by building a new 1,000 km line through Iraq or rehabilitating the Kirkuk-Baniyas route at Iran’s expense. The project, with a planned capacity of 1.25 million bpd, was reportedly destined for the Lebanese coast. Russia later supported the initiative and held meetings in Baghdad to advance it. No action followed until Iraqi Prime Minister Mohamad Shia’ al-Sudani visited Damascus in July 2023 to discuss reopening the pipeline. Iraq’s government spokesman later confirmed Baghdad’s readiness to engage.