After more than a decade of isolation, Syria’s investment landscape is being reconfigured. Dozens of new Memoranda of Understanding (MoUs)—many driven by Gulf and Turkish actors—signal an emerging realignment. Yet this shift should not be overstated: most commitments remain MoUs, with very few progressing toward implementation.

Building on our earlier analysis of MoU values, ownership structures, and implementation risks, this article turns to the geopolitical dimensions of this new investment wave. It compares pre- and post-Assad models of foreign engagement to show not only who is investing, but how—and what this reveals about Syria’s evolving economic landscape.

Mapping New Investment: A Diverse Geographical Distribution

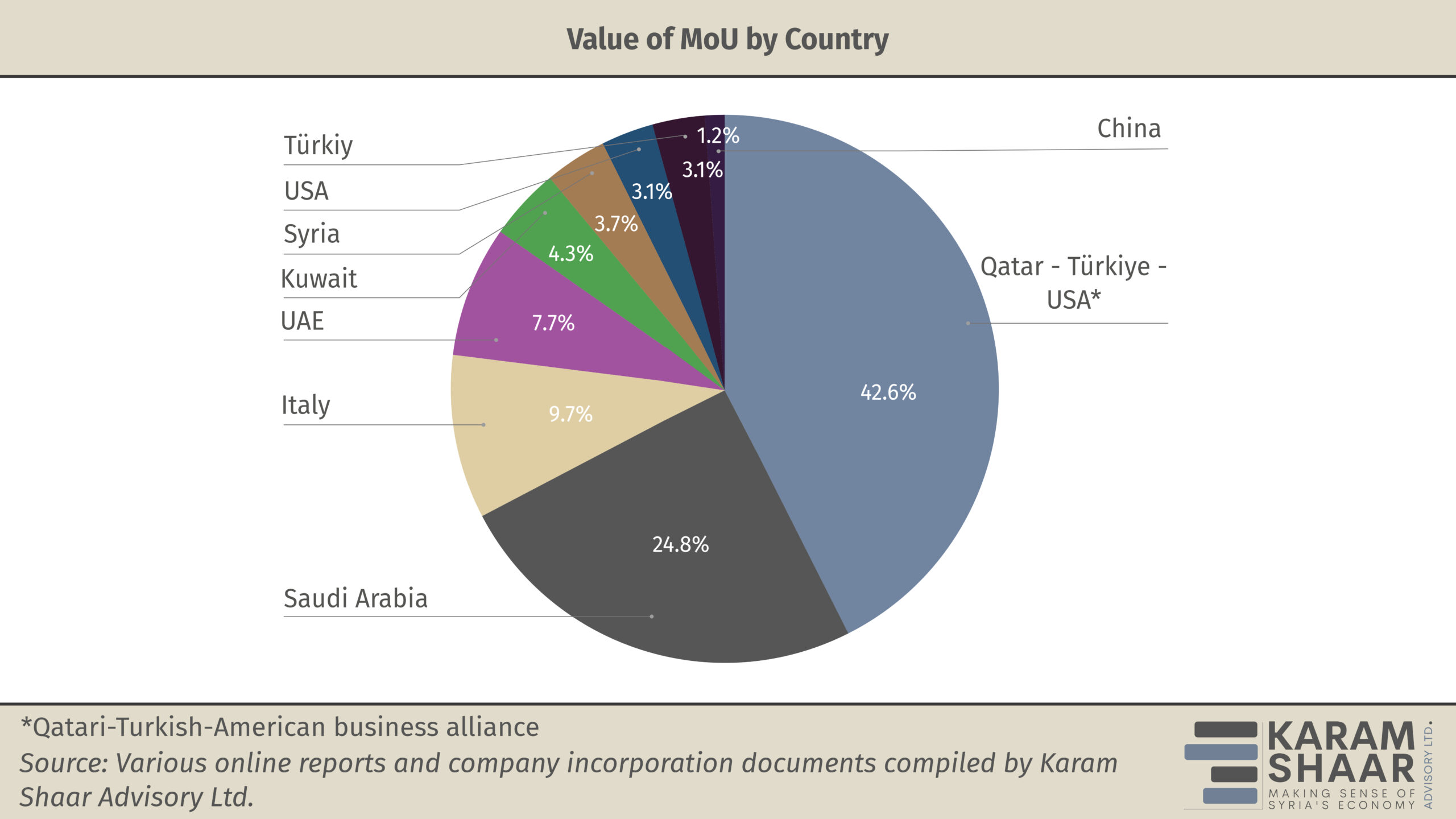

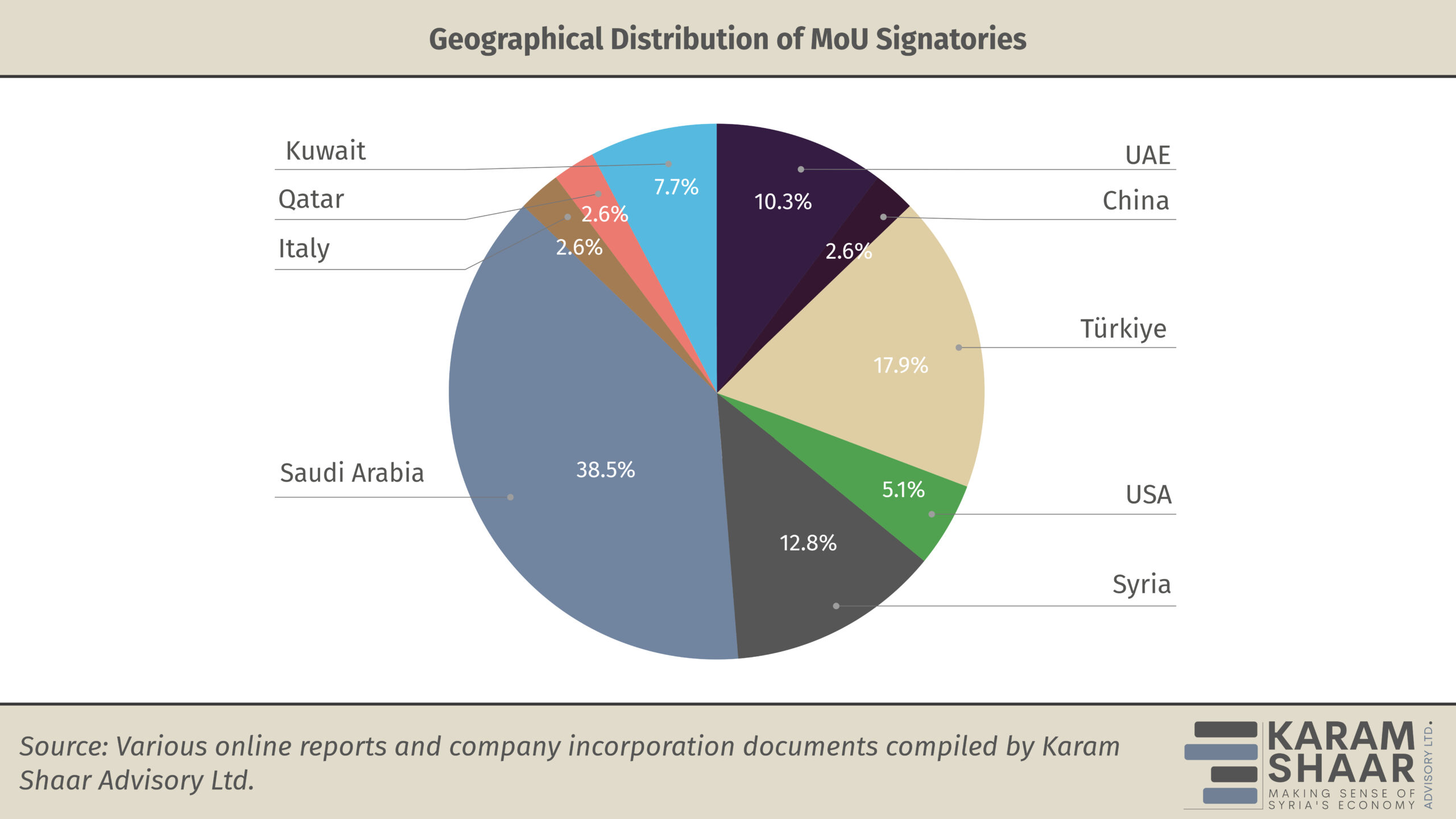

Based on our review of 40 MoUs, the disclosed portions of these agreements amount to USD 25.9 billion—slightly below the USD 28 billion figure announced by Syrian President Ahmed al-Sharaa during the Future Investment Initiative in Riyadh, a discrepancy expected given the absence of published values for several MoUs. The geographical distribution of these agreements shows how regional influence in Syria is being reshaped. Gulf actors now dominate the landscape: Saudi Arabia leads in the number of MoUs signed and ranks second in value, with Saudi firms signing USD 6.4 billion in MoUs during the Syrian–Saudi Investment Forum. The UAE follows with four companies, though only one disclosed its value—the USD 2 billion Damascus Metro project with Al-Wataniya Company. Kuwait comes next with three firms, two of which announced a combined value of USD 1.1 billion, while the third, the ‘Boulevard Homes’ project, disclosed no figure.

Qatar’s engagement takes a different form, driven by a Qatar–Turkish–US consortium led by UCC Holding, which signed two MoUs worth USD 11 billion—about 43 percent of all announced investment this year. The consortium includes Power International Holding, a US-linked firm reportedly tied to the same Qatari corporate network, indicating a financial–logistical structure rather than a broad multinational partnership. Another US-linked company, Classera (EdTech), signed strategic agreements in August 2025 with Syria’s Ministries of Communications, Education, and Health.

Domestically, several Syrian companies have also signed MoUs, but opaque ownership structures and weak governance raise questions about whether many of these deals represent real investment.