In our previous issue of Syria in Figures, we mapped the investment memoranda of understanding (MoUs) signed by the Syrian government after Assad’s downfall, outlining their geographic and sectoral distribution and the barriers hindering their implementation.

Building on that analysis, this article turns to the investors themselves. After documenting MoUs worth at least USD 25 billion, it has become critical to assess who these companies are and the operational and financial risks they pose. This article focuses on high-risk firms and how their involvement could affect the credibility of Syria’s reconstruction process.

Risk Analysis of the Investing Companies

All 40 for-profit firms officially named in credible media and news outlets were included in our assessment. MoUs linked to nonprofit development projects are outside the scope of this review.

The evaluation applied three criteria:

- Institutional Maturity: measured by founding date and market experience.

- Transparency and Disclosure: the availability of public information such as official websites, financial reports, and activities.

- Governance and Leadership: assessed through organizational structures, executive profiles, and accountability mechanisms. A company received higher scores where leadership details and governance frameworks were publicly accessible and verifiable.

We gathered data through company websites, financial disclosures (where available), social media, independent investigations, and verified media reports. All information was cross-checked across multiple sources, with particular attention to confirming that each company existed and was operational.

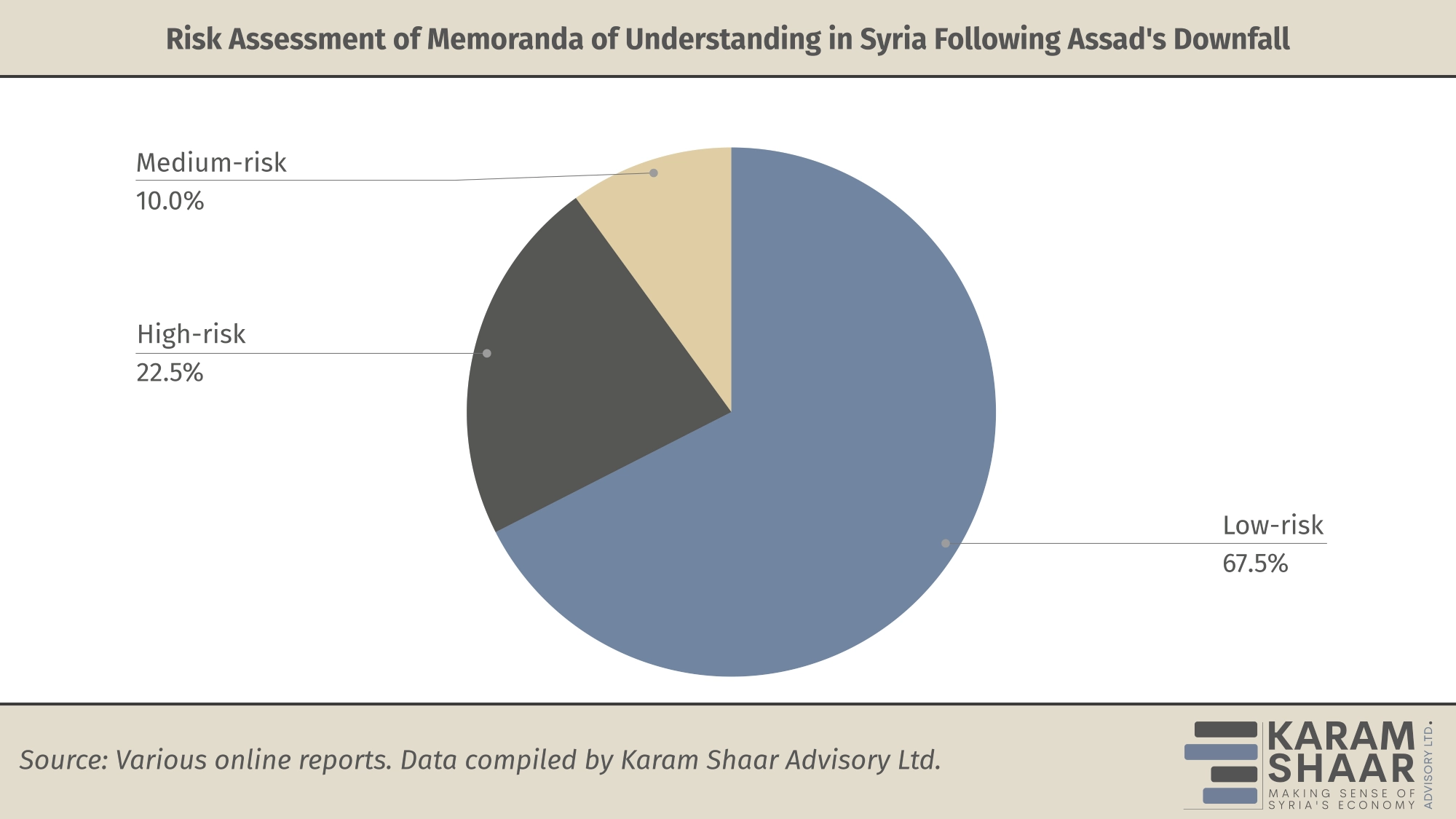

Each company was then scored from 0 to 6 points under the three criteria. Overall scores of 0–2 indicated low risk, 2–4 medium risk, and 4–6 high risk. While limited in scope, this scoring provided a consistent and transparent basis for comparison.

The results show that most firms fall within the low-risk category, accounting for 67.5 percent of the sample. Ten percent were assessed as medium-risk and 22.5 percent as high-risk. This distribution is reassuring, as most signatories exhibit reasonable credibility and institutional stability.

In particular, firms from the Gulf and Türkiye form a solid core of reputable players with proven records in international markets. A notable example is the Qatari–Turkish alliance, which brings together four companies: UCC Holding from Qatar, Cengiz İnşaat and Kalyon İnşaat from Türkiye, and the US-registered Power International Holding.

Despite the apparent proximity between HTS and the Al-Khayyats—raising transparency and favoritism concerns—the Qatari–Turkish alliance has emerged as one of the most credible large-scale commitments to Syria’s reconstruction. It has signed two MoUs with the Syrian government: the first, valued at USD 7 billion, focuses on energy sector development; the second, worth USD 4 billion, entails constructing a new airport in Damascus. Together, these projects, totaling USD 11 billion, underscore both the financial weight and the strategic vision of this partnership, positioning it as a cornerstone of Syria’s post-conflict recovery. The broader implications of such alliances and their role in reshaping Syria’s economic landscape will be explored in the next issue, which will map emerging foreign investment networks under new MoUs.

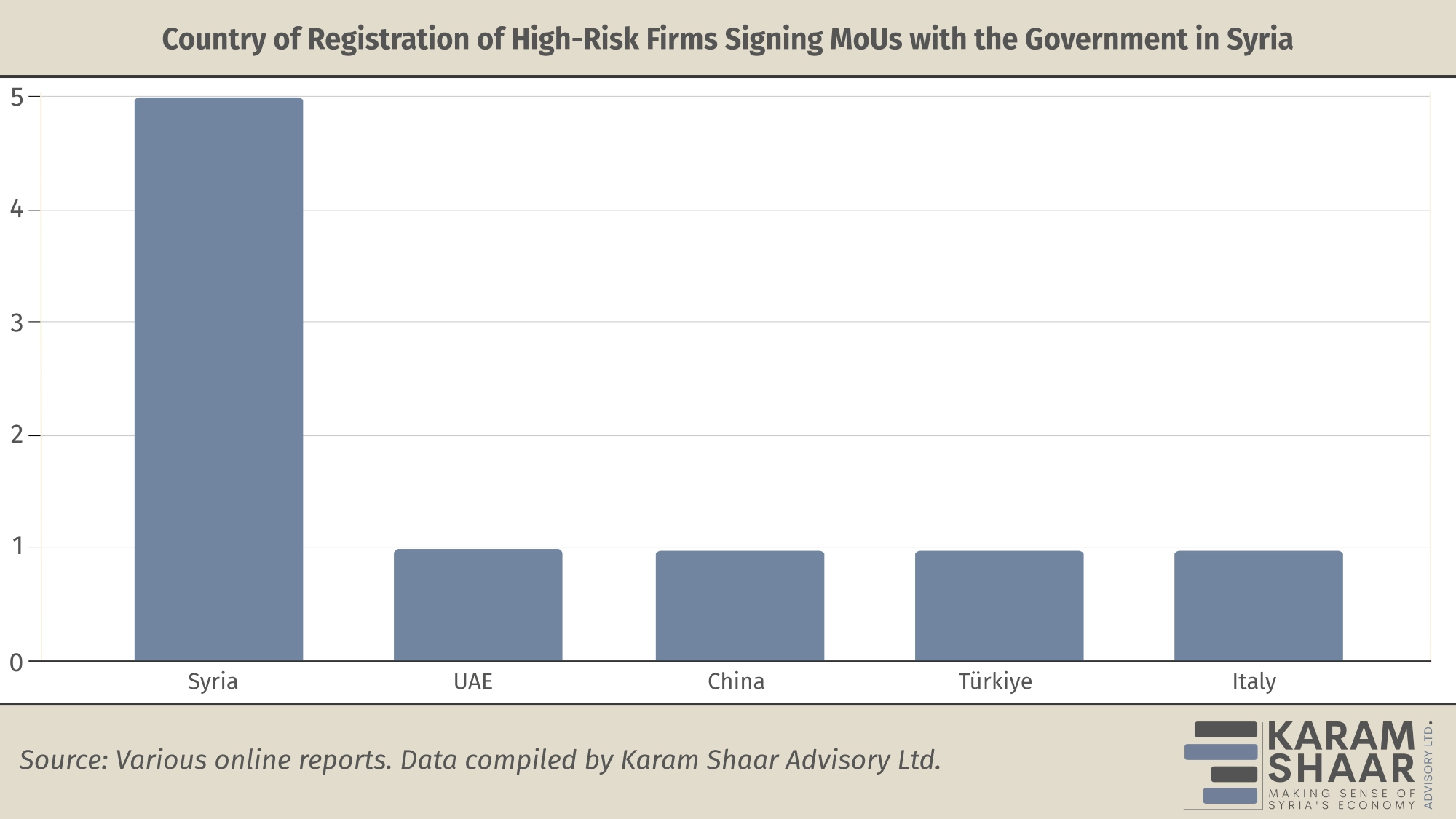

More than one-fifth of the companies are considered high-risk and require closer scrutiny. These firms threaten the credibility of reconstruction efforts and undermine investor confidence in Syria’s new investment framework. Their participation introduces significant risks, including project cancellations, delays, resource misallocation, and substandard execution. It also increases the likelihood of corruption and political favoritism. Such outcomes erode public trust and deter credible external investors from engaging in Syria’s recovery.

None of the high-risk companies possesses an official website. Their digital presence is limited to scattered social media pages, while six companies had no traceable footprint at all. This lack of visibility raises serious questions about their actual existence and capacity to execute multi-million-dollar projects, casting doubt on both their credibility and the sustainability of their commitments.

Companies with Massive Contracts and Missing Facts

The Damascus Towers Project (valued at USD 2.5 billion) illustrates the risks of weak corporate vetting and the absence of transparent tendering processes and formal award procedures. The contract was granted to the Italian company Ubako-I S.R.L, founded in 2022 with a registered capital of only EUR 16,000 (about USD 17,400) and a single employee. Official records show 2022 revenues of just EUR 209,000 (about USD 228,000) and losses of EUR 3,300 (about USD 3,600). The company’s declared specialization is elevators and construction materials—far removed from the requirements of a megaproject such as Damascus Towers.

Official Statements Confirm the Problem

Lack of transparent competitive bidding and formal tendering processes allows for inappropriate contractor selection in major infrastructure projects. The mismatch between project scale and company capacity necessitates enhanced due diligence on contractors’ financial resources, technical expertise, and track record. Weak governance, insufficient stakeholder engagement, and a lack of transparency in decision-making can jeopardize project viability by fueling resistance, regardless of contractor quality.

Syrian Economy and Industry Minister Dr. Nidal al-Shaar acknowledged in a recent press interview the existence of problems with some companies that signed memoranda of understanding. The minister confirmed that “not all memoranda of understanding lead to contracts,” noting that the government will conduct due diligence and terminate dealings with any “deceptive or non-serious” company.

At the same time, the Lebanese newspaper Al-Modon, citing its own sources, reported that the General Secretariat of the Syrian Presidency has instructed a comprehensive review of all signed memoranda of understanding. According to the report, any memorandum not translated into concrete implementation by 13 September 2025 would be considered void without future state obligations. However, this information has not been officially confirmed by Syrian authorities.

The minister’s statements and these press reports raise important questions about the effectiveness of the current screening mechanisms. If, as the minister asserts, the government performs thorough due diligence, how did companies such as Polidef and Ubako manage to reach the stage of signing billion-dollar contracts despite clear indicators of their limited capacity?

Such a pattern suggests that the government may have fallen into a populist trap, prioritizing the announcement of large-scale foreign investments to demonstrate economic recovery and international confidence, without adequately vetting the actual capacity and credibility of the contracting parties.

The situation underscores a fundamental challenge for the Syrian government: balancing the urgent need to attract investment under economic sanctions with maintaining rigorous standards to ensure the quality and credibility of contracting companies, while avoiding the temptation to prioritize headline-grabbing announcements over substantive due-diligence processes.

Looking Ahead

The Syrian government faces a difficult position: it urgently needs reconstruction investments yet has limited options among credible firms willing to operate under current conditions. This context explains, though does not justify, how smaller or questionable companies secured major contracts.

The government must establish clear due-diligence standards, including verification of companies’ financial and legal records and confirmation of their actual existence and operational capacity. These standards should mandate the submission of audited financial statements, proof of completed projects, and evidence of technical expertise relevant to proposed work.